Jim Simons and the Making of Renaissance Technologies

The philosophy and lessons behind "a moneymaking machine like no other" (with a cumulative trading profit of $100B +).

Thanks for subscribing to SatPost.

Today, we will talk about how Jim Simons built the most successful hedge fund ever: Renaissance Technologies.

Also this week:

Roaring Kitty and GameStop

Google vs. OpenAI

…and them wild memes (including King Charles)

In the previous newsletter, I shared news that Jim Simons had passed away at the age of 86 and mentioned that I would write about the legendary investor. I had intended to publish a longer piece after more research, but enough of you readers pinged me for details that I decided to update a Twitter thread that I wrote in 2021 about Simons and Renaissance Technologies ("RenTech") to post this week.

Here is how Simons explained his career: "I did a lot of math. I made a lot of money, and I gave almost all of it away. That's the story of my life."

The definitive source on Simons is The Man Who Solved The Market, a (highly recommended) book from 2019 written by author and Wall Street Journal writer Greg Zuckerman. Simons rarely spoke on the record but he spent hours with Zuckerman, who shares a lot of RenTech data in his book.

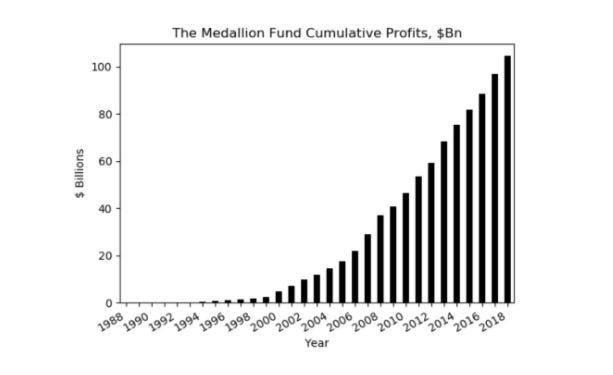

The iconic Medallion Fund — which was created by Simons' investment firm —made an astonishing $100B in trading profits from 1988 to 2018 (if combined with my portfolio, the figure grows to $100,000,000,007).

To understand how, let’s discuss:

The Making of Renaissance Technologies

The Medallion Fund’s Secret Sauce

Simons’ 5 Life Principles

***

The Making of Renaissance Technologies

At the age of 40, Jim Simons left a renowned career in math to start what would become Renaissance Tech ("RenTech"), the most successful hedge fund ever.

The crown jewel of RenTech is the Medallion Fund. Launched in 1988 — a decade after Simons stared investing — the fund posted an annual gross return of 66% for the next 30 years (39% after fees). A single $1 invested in 1988 would be worth $14m by the end of that run and even more now as the fund is still going strong.

This is a story of genius, talent management and the birth of quant trading. But also a story of how difficult it can be to beat markets.

Before creating what Bloomberg dubbed a “moneymaking machine like no other”, Simons had lived a full life and as a legendary mathematician.

1938: Born in Newton, Massachusetts.

1958: At 20, he graduates from MIT with a Bachelors in Math.

1961: At 23, he graduates from Berkeley with a PhD in Math.

1964-1968: He works as a codebreaker for the NSA as part of the Institute for Defense Analyses. He is later fired from the NSA/IDA for telling Newsweek magazine about his opposition to the Vietnam War.

1976: He is awarded the Oswald Veblen Prize for Geometry (He also founded the Chern-Simons form, which is a theory widely used in quantum computing.)

1968-1978: He serves as the Chair of the Math Department at Stony Brook University, where he builds and leads one of the nation's top math faculties.

While Simon's background is heavy on the academic side, he always had an interest in making money. Why? Mostly as a way to ensure his professional freedom and allow him to pursue his own interests. (Simon's need for financial independence is often highlighted by a story about his lifelong smoking habit. As an anecdote in a New Yorker profile tells it, "Simon smokes constantly, even in enclosed conference rooms... he pointed out that, whatever the fine for doing so is, he can pay it.")

In his early 20s, Simons took a $5k wedding gift and learned to trade soy futures. After making a small profit, he gave up trading for decades. But another business venture would provide the seed funds for Renaissance Technologies: during his graduate days at MIT, Simons motorbiked from Boston to Bogotá with a Colombian classmate, who then started a business in the country and Simons invested.

Fast forward to the 1970s. His Colombian classmate scored an exit, which provided Simons with extra funds to start trading commodities while running Stony Brook’s math department. The side investing was good enough that Simons — also going through a divorce — decided to leave academia and launch his own money management firm in 1978: Monemetrics.

At the time, there were two main investment approaches: 1) fundamental (understanding and forecasting an asset based on key drivers); and 2) technical analysis (studying price charts).

Simons' strategy was to place a "fundamental lens" on currencies (e.g. tracking supply and demand). While Monemetrics experienced moderate success, Simons referred to the emotional swings of day-trading as "gut-wrenching". He desired a more systematic method, and thus set out to create a third approach: using complex mathematical models to identify signals that anticipate price movements (another distinct approach being the firm's first office location, a Long Island strip mall which is over 50 miles away from the Wall Street toomfoolery).

As a former codebreaker, Simons believed that "there are patterns in the market" and that he could "find them". The job of finding these patterns was not for MBAs, but for PhDs and scientists. His first hires were former colleagues from Stony Brook and the NSA.

In 1982, he renamed the firm Renaissance Technologies.

It took years, but RenTech created a 3-step process to find "statistically significant moneymaking strategies" (aka signals):

Find an anomalous pattern in historic pricing data

Be statistically significance, non-random and consistent over time

Be somewhat explainable

These signals were called "tradeable effects". While many are now common in quant funds, RenTech did them first and did them (alot alot alot alot alot) better.

Some notable trading themes were:

Mean-Reversion: Prices tend to revert after moving higher or lower (one RenTech employee said “we make money from how others react to prices”).

Trending: RenTech accurately predicted how long an investment would continue to move in a trend (whether up or down).

Economic Releases: Prices for some assets fell right before and gained right after an economic release (e.g. labor statistics).

Seasonality: Monday’s price action was similar to Friday’s while Tuesday’s saw a reversion to previous trends.

Trader Habits: Commodity traders would sell a position on Friday so they wouldn’t hold an asset if something happened on the weekend.

In 1988, the single trading model — which would always remain a single model — officially became the Medallion Fund (named after one of Simon's math awards).

The first fund was $20m.

Early returns were meh…

1988: +16%

1989: +1%

...but then BOOM GOES THE DYNAMITE:

1990: +78%

1991: +54%

1992: +47%

In 1993, Simons decided to stop accepting outside money for the Medallion Fund. He also increased the fees for investors, including employees. Everyone agreed to the new terms, which resulted in fees going from "5% management and 20% performance" to "5% management and 44% performance".

A 44% performance fee may seem excessive, but Renaissance Technologies ultimately became owned solely by its employees and alumni. This was a smart incentive structure that helped attract and retain top talent. The high fees also allowed younger employees to be compensated well as they took on more responsibilities while other members retired or left the company.

At the same time as the change in management fees, Simons made personnel moves that would define RenTech for decades. He hired a number of scientists and PhDs from IBM’s Thomas Watson Research Centre. Its speech recognition unit yielded RenTech's future Co-CEOs: linguists Rob Mercer and Peter Brown.

As an IBM colleague observed, “Speech recognition and translation are the intersection of math and computer science.” Mercer and Brown actually pitched IBM to apply computational stats to manage its $28B pension. IBM said "no" and they (along with others) joined Simons.

RenTech's poaching of the IBM team opened up the world of tradable assets. Up until that point, Medallion had gained nearly all of its profits from currency and commodity futures. With the incorporation of algorithm design and coding skills from IBM, the fund was able to add thousands of equities to its model.

This was a proto-LLM in many ways:

Mercer and Brown studied language as a probability challenge (rather than fixed rules).

Their IBM speech recognition models used n-grams to predict the likely next word in a sequence (similar to how LLMs do next-token prediction).

They led IBM’s famous machine translation Candide project, which used the Canadian government’s bilingual corpus of text to train a model based on probability. They realized the more training data led to better results (comparable to scaling laws with LLMs).

The IBM injection allowed the fund to increase its size…and make better stock predictions.

The fund never grew too large, however, as the short-term nature of its strategies restricted how much money could be invested. The fund's current size is capped at ~$10B, with annual profits being distributed to alumni and over 300 employees, 1/3rd of which hold PhDs (I’ve left out many of these names from the story, which is another another reason y’all should check out Zuckerman's book).

The limited fund size and the fact that the money barely compounds make the total cash generated — over $100B in profits — all the more remarkable. After deducting its large 5/44 fees, the annualized return for Medallion from 1988 to 2018 was an outrageous 39% (compared to an even more impressive gross return of 66%).

Interestingly, the fund only won 50.75% of its trades. An army of top PhDs are basically a coin flip in trading. Markets are hard AF (most should just buy and hold).

Mercer has perhaps the most quotable quote of the entire Renaissance Technologies story: “We’re right 50.75% of the time, but we’re 100% right 50.75% of the time. You can make billions that way.”

The year-by-year return chart is insane (I’m running out of superlatives to describe these numbers):

Add it all up and the Medallion Fund's returns (1988-2018) are absurd:

since 1990, its worst year is +32%

In 24 of the 31 years, it was s up at least 50%

It had three 100%+ return years, all in the worst market conditions: 2000 (+128%), 2007 (+137%) and 2008 (+152%)

In the next section, I’ll walk through a bit of RenTech’s secret sauce.

But before we dig into that, here are four more details of the RenTech story worth flagging.

First, when you make $100B in trading profits — a problem that I do not have — the IRS is going to take a very close look at your taxes. In 2021, RenTech paid $7B to settle a dispute over how the firm classified its trades over the decades. The gist is that RenTech was booking its derivative trades under "long-term capital gains" when they were actually short-term gains (which are taxed at a higher rate). That is one painful back-tax payment.

Second, Simons officially retired from RenTech in 2009 but remained involved in high-profile management issues. A lifelong Democrat, he had to deal with controversy surrounding Robert Mercer, one of Donald Trump's top donors in 2016. Mercer stepped down from Renaissance Technologies in 2017 (Peter Brown remains CEO).

Thirdly, RenTech has been offering institutional funds to outside investors since 2005. It started with the Renaissance Institutional Equities Fund (RIEF) and has since launched two other funds. Together, these funds manage over $50B. However, their performance has been really lacking in recent years with the funds significantly underperforming the S&P 500. Translation: the RenTech magic has its limits.

Fourthly, I'm sure some of you are thinking, "Should the world's top math and physics PhDs be spending their time on a money-making machine like no other?" It's a fair question. However, I'm not exactly the most qualified person to discuss how society should allocate time and capital. I once spent 47 minutes arguing with Uber Eats over the delivery fee for a $68 order of McDonald's I made at 11pm because I saw someone eating a Big Mac on a Netflix show and got hungry. There’s clearly a continuum of how to apply one’s otherworldly talents. In my estimation, making a fortune at RenTech is neither the worst nor the best application of said skill.

Anyway, feel free to share your thoughts on that but let’s move on.

***

The Medallion Fund’s Secret Sauce

How was the Medallion Fund able to pull it off?

I mean, no one really knows. Even the RenTech team doesn’t fully know what’s up with the model. And anyone who knows even a modicum of how it works isn't sharing the information because they've signed a fat NDA and have zero interest in missing out on those sweet distributions. Some funds did poach ex-RenTech employees, but lawsuits were filed. In other words, the actual secret sauce remains secret.

Still, there are some high-level details that help to explain the fund’s wild performance. Here are 10 of them drawn from Zuckerman’s book and also this series of fireside chats with MIT’s Andrew Lo.

1. Simons is an incredible leader

From his days at Stony Brook University, Simons has long experience managing intellectual egos. His academic credentials and trading chops earn universal respect.

People with Simons’ brain usually don’t have that level of EQ and people with that level of EQ don’t usually have his brain. Per Bloomberg, Simons is the “benevolent father figure” that inspired “super nerds to stick together.”

2. Culture for top talent

One primary aspect of Simons’ job was to establish a desirable place for high-level scientists to be motivated to work. Here are his thoughts on developing RenTech's culture:

“The model has been first hire the smartest people you possibly can. I think we have the top scientists in their fields [astronomy, physics, math]. And then, work collaboratively. We let everyone know what everyone else is doing.

Now, some firms that do have these systems, they have little groups of people and they’ll get paid according to how [each of their systems] goes up.

We have one system. And once a week, at a research meeting, if someone has something new to present, it gets presented. It gets chewed up and everyone has a chance to look at the code. Anyone can run the code and see what they think.

So, it’s a very collaborative enterprise, and I think that the best way to accelerate science is people working together. It’s a very nice atmosphere. It’s fun to work there. People get paid a lot of money, so there’s very low turnover.”

Another aspect of collecting the best talent is that Simons had everyone pulling in the same direction by contributing to the single model.

Academia can be very zero-sum, with PhDs fighting over the same honors and pool of grant money. Similarly, many investment firms pit fund managers against each other, with top performers receiving money and accolades.

At RenTech, everyone wins when the one trading model is successful. This aligns incentives and fosters cooperation.

3. Never override the computer

The driving logic behind RenTech was to create a systematic trading approach that wouldn't be compromised by human emotion. The Medallion Fund has performed the best during volatile times, because it lets the model run while everyone else is losing their minds.

Per Simons:

“The only rule is that we never override the computer. No one ever comes in any day and says the computer wants to do this and that’s crazy and we shouldn’t do it. You don’t do it because you can’t simulate that, you can’t study the past and wonder whether the boss was gonna come in and change his mind about something. So, you just stick with it, and it’s worked.”

Apparently, RenTech did override the model once during the “Quant Quake” in 2007 but it was an exception that proves the rule.

4. Data edge

RenTech's unofficial motto is "There's no data like more data." It was a pioneer in gathering and cleaning data. The team collects data of various types, such as weather, prices, and newspaper blurbs, for its model earlier than most other funds. Today, its system ingests one terabyte of data per year in order to improve the trading model.

5. Great execution

RenTech makes 150k-300k small trades per day, with holding periods of ~2 days. A crucial aspect of their trading model is accurately estimating the bet size to minimize any negative effects on the trade (which RenTech refers to as "slippage" for transaction costs).

6. "Don’t ask why"

RenTech believes that market participants vastly underestimate how many variables drive an asset. The team rarely offers hypotheses. Instead, they let the data speak and if a signal works — even if they don't fully understand why — they will trade it.

7. Stealth trading

When RenTech finds a market inefficiency, it goes to great lengths to not give away the trade.

Here is an excerpt from The Man Who Solved The Market:

“If Medallion discovered a profitable signal — for example that the dollar rose 0.1% between 9am and 10am — it wouldn’t buy when the clock struck nine, potentially signalling to others that a move happened each day at the time. Instead, it spread its buying out throughout the hour in unpredictable ways, to preserve its trading signal. Medallion developed methods of trading some of its strongest signals ‘to capacity,’ as insiders called it, moving prices such that competitors couldn’t find them.”

8. Extreme diversification

The move into equities allowed RenTech to trade in many more assets (and deploy up to $10B per year). At any one time, the Medallion Fund can have 4k long and 4k short trades.

Such a diversified portfolio reduces overall risk, giving RenTech access to...

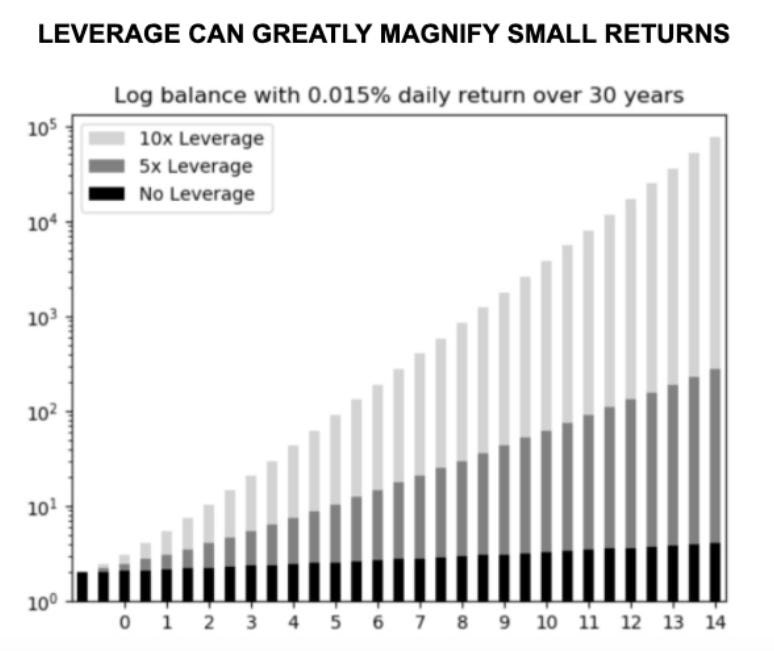

9. …Leverage

Having built a trading machine with the best data and execution combined with diversification, banks (e.g. Deutsche, Barclays) are happy to lend RenTech money.

Medallion typically leverages 12.5x (and often goes as high as 20x). Without leverage, its returns are comparable to those of the S&P 500.

As the late Charlie Munger once said, “Smart men go broke three ways: liquor, ladies and leverage.” RenTech’s next-level risk management — and trading record — gives its partner banks confidence to provide leverage. Few other firms will ever get such a long leash (and even if they did, they wouldn’t know how to handle it properly).

10. Don't overpay for graphic design.

Alright, this detail wasn't in The Man Who Solved The Market, but I have to point out that Renaissance Technologies and Berkshire Hathaway — two of the greatest investment firms ever — have the dustiest websites in existence.

I know correlation doesn't always equal causation, but keep these landing pages in mind if you're considering building a $100B+ investment management operation (side note: it looks like Renaissance Technologies dipped into that cash pile and slightly upgraded its website in the past few years).

***

Simons’ 5 Life Principles

In the final decade of his life, Simons (and his wife Marilyn) were primarily focused on philanthropy. Through their Jim Simons Foundation and the Flatiron Institute, the Simons donated billions to scientific research in the search for signals, specifically in the fields of math, astrophysics, biology, and quantum physics.

“I just made the money and Marilyn gave it away,” Simons said of his philanthropic efforts.

For all his success, Simons says "luck plays quite a role in life". He's also dealt with very bad personal luck: losing two sons in separate accidents. When asked about the losses, Simons once remarked to a colleague, “my life is either aces or deuces.”

Taken all together, Simons has laid out his five life principles during lectures in recent years. Frederik Gieschen has a great breakdown of each principle and I’ve included key quotes from Simons below:

Don’t run with the pack: “Try to do something that’s original.”

Collaborate with wonderful partners: “Find someone that’s smarter than you that can leverage your efforts.”

Be guided by beauty: “It’s easy to find a nice aesthetic in a math formula, but you can find beauty in many other enterprises. A well-run business is kind of a beautiful thing.”

Persistence: “Something that's really worthwhile can take a lot of time to come to fruition and you ought to have patience. If you believe in something, just stick with it.”

Hope for good luck!

These principles are much more applicable than trying to replicate the Medallion Fund’s $100B secret sauce. Countless investors have tried for decades but failed to reach the same heights. Even RenTech can’t replicate a fraction of the performance for its institutional funds.

Remember, it’s “like no other”.

My main takeaway from the story is how it’s never too late to start something new. Simons gave up his academic career at 40 and became arguably the greatest investor ever.

Anyone can try creating something using principles #1 (be original) and #2 (finding wonderful partners). Then, build it with principles #3 (be guided by beauty) and #4 (be persistent) while keeping in mind that #5 (hoping for good luck) is largely out of our control. However, if you have the other four principles in place, it's a solid start... at any age.

Why are you seeing this ad?

Because I co-founded an AI-powered research app called Bearly AI. And I really like putting blue buttons in this email.

If you press this blue button below, you can save hours of work with AI-powered tools for reading (instant summaries), writing (the new GPT-4o, Claude Opus 200K) and speech-to-text transcription tools (Scribe, Whisper).

It’s all available in one keyboard shortcut (and an iPhone app). Use code BEARLY1 for a FREE month of the Pro Plan.

Links and Memes

Roaring Kitty and GameStop are Back: Speaking of legendary investors, Keith Gill is a 37-year old financial analyst from Massachusetts. You know him as Roaring Kitty or u/DeepF**kingValue and the world’s most famous CFA. He was the face of the Reddit and Wall Street Bets retail trading mania a few years back.

After posting his bull case for GameStop and YouTube non-stop in 2020 and 2021, Gill — who turned $53k of GME stock into as much as $48m — went quiet for nearly 3 years. Until last Sunday, when his X account posted a cartoon of a guy leaning forward in his chair about to play a video game on hard mode. Since then, he’s posted over 50 videos of popular film clips and cultural memes (Ferris Bueller, ET, Fast & Furious, Ocean’s 11, Seinfeld etc) suggesting that he’s back in the game.

No one has any idea what is going on but the internet translated the memes as a sign that GameStop was back. The stock went from a $5B market cap to as high as $15B and is now back to $6B. AMC — the theatre chain and other major meme stock from 2021 — also saw its stock more than double from $900m to $2B and is now back to $1.3B.

Bloomberg’s Matt Levine has a 20-minute segment on the Money Stuff podcast going through some theories including:

Did Roaring Kitty sell his X account? I hope not.

Is this the best way for Roaring Kitty to monetize his brand? If he bought a bunch of call options before tweeting that first post in 3 years knowing he would make the market pop, then he probably made dough. I’m guessing he’s still holding a large GME position, either way.

Is this insider trading? Probably not, because he’s a public shareholder and none of the memes actually mention material GameStop information.

Who won from this madness? AMC had a share offering during the brief meme stock pump and was able to pay down some debt; GameStop also initiated a share offering and can raise some money. But the real winner is the internet and meme lovers.

A few thoughts: First, SatPost reader Chris M. notes that the public reaction to Roaring Kitty's return shows that Gill may have some of the most unused political capital in America. Future Massachusetts Senator?

Second, the internet is moving way too fast. We’ve already forgotten about the Drake vs. Kendrick beef and the 2024 version of GameStop mania feels like it’s already over after 72 hours. Unless the Roaring Kitty account — which is hopefully still controlled by Gill — announces a new stock position, everyone will soon move on.

Finally, a few hedge funds — after learning zero lessons from 2021 — were shorting GameStop and lost over $1B on their trades after the renewed mania. With thousands of equities in the world, why short one that could potentially move 50-100% based on a single image like this?

Consulting Firms and the Middle East: The Financial Times had an article about how consulting firms (Bain, Accenture, Deloitte, McKinsey) were milking Middle Eastern governments on advisory contracts for decades. However, the oil-rich governments are apparently getting stingier with the consulting firms. Anyway, the most interesting comment on the topic came from investor Kaushik Subramanian, who explained how McKinsey employees considered opportunities in the Middle East:

When I joined McKinsey from business school you had two options that you could put on the form:

1. Go to London, grind more, get paid significantly less and pay more tax. But work on more interesting projects/clients

2. Take a 10 year bet — work in the Dubai office for $250K tax free starting + bonus, and in 10 years you'd retire as AP/Partner with decent money to move back to India/Lebanon/Italy (these were the 3 main nationalities). Literally everyone knew this. Work-life balance was generally bad, but you'd fly to Saudi every Sunday (work week Sun-Thurs), fly back on Thursday and during that time stay at the Ritz in Riyadh. I knew one Lebanese AP who was 'based' in Dubai but only stayed at SPG properties for 10 years - no flat/apartment! He is now retired, SPG (now Bonvoy) platinum for life which used to be quite a flex.

***

Some other baller links:

The Economics of Salad: A salad from Sweetgreens costs $15 but the health food chain still somehow loses money on each order. Food and labor is about $12 and there’s another $5 in admin overhead, which puts Sweetgreens in the red. Sherwood News says Sweetgrren is trying to improve profitability by selling higher-margin steak and introducing more robotics. I suggest just marking avocados up by 500%, since Chipotle’s guacamole has completely warped what society thinks is a reasonable price for an avocado.

Scottie Scheffler: If you’re a golf fan and are following the story of Scheffler getting arrested before the PGA Championship, here is a thread of 25 memes for you.

Google vs. OpenAI: Both tech firms had keynotes that hyped the consumerization of AI tools. Om Malik compares the focused OpenAI keynote for its new GPT-4o model (“o” stands for “omni”, meaning the model accepts images/texts as inputs and has a very smooth conversational UI) to Google’s I/O developer presentation, which was more of a spray and pray approach (basically showing that Google is fast following by shoving AI down every crevice it has including Search, Sheets, G-Mail, Docs, Slides). Google has all the resources, so this “shove it in every crevice” strategy isn’t the worst idea but does show how the $2T tech giant lost its grip on the AI narrative.

Also check these out:

OpenAI demos real-time translations

Khan Academy’s Sal Khan demos an OpenAI tutor

Both Google and OpenAI showed chat interfaces with low latency (think the film “Her”). Rex Woodbury has a good piece on “AI's Communication Revolution”.

Google’s Demis Hassabis demos a Google AI assistant that can see, hear and read with super low latency

...and them fire posts (including King Charles' first official portrait since his coronation...a lot of people thought it looked "hellish," but the aggressive red hue definitely screamed "marinara sauce" to me).

Great read. The man is a Wall Street Legend. He was a great trader in many ways of course, but it’s amazing to see how he protected his capital during the bear years. That provided tremendous alpha for his fund.