MicroStrategy's $37B+ Bitcoin Bet (Is Just The Start)

How Michael Saylor turned a B2B software company into one of the world's largest owners of Bitcoin.

Thanks for subscribing to SatPost.

Today, we’re talking about MicroStrategy, one of the wildest business or tech stories in 2024 (an $89B SaaS software company holding $37B of Bitcoin).

Also this week:

Apple TV+’s weird $20B+ strategy

My Gladiator II review

The Dermatology Boom

…and them fire posts (including Drake)

PS. Check out the newest episode of my podcast Caffeinated Deep Dives, which is about the history and business strategy of Trader Joe’s (Apple, Spotify, YouTube).

We need to talk about MicroStrategy.

It’s a $89B publicly-listed software company that holds $37B of Bitcoin (BTC) on its balance sheet. Founded in 1989 by Michael Saylor as an enterprise B2B SaaS provider, MicroStrategy has conducted one of the most jarring corporate pivots in corporate pivot history.

Over the past 5 years, MicroStrategy has returned a massive +2,478% and even outperformed the monster known as Nvidia (happily, I own a combined 7-figures in these two stocks: $00.00000).

Since mid-2020, MicroStrategy has spent ~$22B to buy 386,700 Bitcoins at an average price of $57k. This position is equal to ~1.8% of the entire Bitcoin supply. At the current BTC price of $97,000, that pot of Bitcoin is worth over $37B. For those keeping track, that means the stock market is assigning MSTR more than a 2x premium over the net asset value (NAV) of its Bitcoin.

Part of this premium is related to the fact that MicroStrategy has identified large pots of investment capital that are demanding Bitcoin-linked financial products (and it’s the only real US-listed public company offering these products at scale).

Let me explain:

Why Did MicroStrategy Pivot To Bitcoin?

MicroStrategy’s Financial Engineering

Saylor’s Long-Term Bet (and Risks)

(Disclaimer: I don’t own MSTR but am long Bitcoin and — for the love of Zeus’ beard — none of this is investment advice).

Why Did MicroStrategy Pivot To Bitcoin?

Anyone that has listened to a Michael Saylor podcast over the past few years should be familiar with MicroStrategy’s Bitcoin story (seriously, he’s done probably over 1,000 hours of interviews while honing his message and I’ve passively digested 42-44% of them while cleaning dishes).

For the uninitiated, here are the broad outlines: Founded in 1989, MicroStrategy eventually rode the DotCom wave to a ~$50B valuation in 2000. After an accounting scandal at the peak of the bubble, MicroStrategy’s stock plummeted and Saylor saw a $6B fortune get wiped out in one day. Over the next two decades, MSTR’s market cap was mostly range-bound between $1B-2B.

In 2019, MicroStrategy’s software business was doing ~$500m a year in sales and $75m in earnings. There was $500m on the balance sheet and the company wasn’t making much headway competing with significantly larger software players such as Microsoft.

During COVID, the US government responded to the pandemic by printing ~$6T (this was 40% of the $15T money supply at the start of 2020; see below for a wild chart). With interest rates at 0% and the money printers going BRRRRRRRRRRRR at the Fed and central banks around the globe, Saylor was concerned that inflation would hit hard and the cash sitting on MicroStrategy’s balance sheet would be massively devalued.

“We had $500m of actual assets and then the government was increasing the currency supply by 20% a year,” Saylor explained on the Iced Coffee Hour podcast in June of this year. “At a 15% [increase in money supply] a year, [MicroStrategy was] losing $75 million of capital value of wealth every year for the $75 million [we’re] winning so…[MicroStrategy had] 2,000 people working as hard as they can, doing 100,000 things right for an entire year to stand still. If inflation is 30% a year, you're running as hard as you can and you're falling backwards. So, another way to say it is everything you do is worthless. Your time is worthless. Your life is worthless.”

With no real option to re-invest its cash into the business, MicroStrategy could return money back to its shareholders by issuing a dividend or conducting a buyback. Saylor saw that as a slow demise and opted to put the cash into an asset that was a dependable long-term store of value. He decided that Bitcoin was the solution to this corporate treasury problem.

Saylor believes Bitcoin is the “biggest innovation in money or property rights” in the history of mankind. The censorship-resistant and distributed protocol combines the internet, semiconductors, energy and economics to create a perfectly-engineered digital money and the apex store of value (with a guaranteed fixed supply of 21,000,000 BTCs that can not be inflated away). In his telling, it’s the solution for 8 billion people and 300 million companies looking for economic sovereignty and freedom.

The key properties that Saylor is optimizing for in a long-term capital asset are scarcity, desirability, portability, durability and maintainability. He believes Bitcoin is the best option considering all these variables. Better than Gold. Better than high-end real estate. Better than trophy art. Better than equities. Definitely better than any fiat currency. Better than [insert your largest portfolio holding; unless that’s Bitcoin, which means you’re on the same page as Saylor].

Whether or not you agree with Saylor’s thesis, there is no denying that Bitcoin has gone from $0 market cap in 2009 to $1.9T in market cap in 2024.

MicroStrategy has been a very visible part of Bitcoin’s rise in recent years. This journey began in August 2020 when Saylor announced that MSTR would be the first publicly-traded US company to make Bitcoin its primary treasury asset. For any shareholders that didn’t want to come along for the ride, MicroStrategy did a buyback at a premium to the stock price.

These two decisions rotated MicroStrategy’s investor base from people holding onto a (slowly) dying software business to people that wanted exposure to Bitcoin. The final tally meant MicroStrategy converted $425m of its balance sheet — out of $500m cash — into Bitcoin. This corporate treasury move soon turned into a raison d’etre for MSTR: Saylor would use MicroStrategy’s existence as a publicly-traded company to issue equity and debt, then use those funds to buy up more Bitcoin.

MicroStrategy was stumbling into a unique business model that solved issues around crypto access:

Ease of investment: A lot of investors interested in Bitcoin aren’t savvy enough to buy BTC on a crypto exchange and self-custody the asset. Also, some high-profile crypto-exchanges ended up screwing regular investors (think FTX).

Regulation: Many pools of capital — pensions, institutional funds, retirement plans — aren’t allowed to invest directly in crypto.

Leverage: Savvy crypto investors and Bitcoin Maxis want to borrow money to increase bets on their Bitcoin positions but this type of leverage isn’t widely available. When the leverage was available, the collateral requirements and cost of capital were onerous. Not many individuals can raise billions of dollars of debt to buy Bitcoin.

MicroStrategy proved a versatile asset to address these obstacles and appealed to large sources of capital. It was a US equity that people could buy on any trading platform. It wasn’t regulated as a crypto company. It was able to lever up by issuing long-term debt and buying Bitcoin (with no risk of getting a margin call).

MicroStrategy’s playbook was commerce 101. Offer people a product they can’t get anywhere else. If I want a Spicy Chicken Burger, a baked potato and chocolate Frosty…there is only one place to go and it rhymes with Fendi’s. In 2020, people that wanted a specific type of exposure to Bitcoin had to go to MicroStrategy. Keep this in mind as walk through the rest of the story.

From Saylor’s August 2020 announcement, MSTR responded to the Bitcoin pivot and its stock price rocketed from an adjusted ~$10 ($2B market cap) to as high as ~$100 ($20B) before retracing back to the teens following the FTX bankruptcy in November 2022.

I know our memories are short but 2022 was just a brutal investing year (the memes were incredible, though). Since MicroStrategy was a levered Bitcoin proxy, it fell harder than Bitcoin did during the market sell-off. Crucially, though, MicroStrategy was never forced to liquidate its Bitcoin holdings.

In 2023, MicroStrategy traded between $20 ($4B) and $60 ($12B)…which takes us to a wild 2024.

MicroStrategy’s Financial Engineering

In January 2024, major financial players — such as BlackRock, Fidelity and Franklin Templeton — launched 11 Bitcoin ETFs, signalling broader acceptance of the digital asset.

Billions of dollars flowed into these ETFs and MicroStrategy’s value proposition for the normie investor seemingly diminished. However, it has become clear that Saylor and his team were formalizing a new product targeted at different pools of capital.

Remember how I talked about those Saylor podcasts? Well, he is a master of analogies and explained MicroStrategy’s new value prop with a few interesting comparisons.

Before I say what these comparisons are, let me flag an analogy from the time that me and the Not Investment Advice podcast team interviewed Saylor in 2022. He dropped so many gems but my favourite was his explanation as to why Bitcoin is the apex method to store value:

Me: What would make you think your thesis on Bitcoin was wrong?

Saylor: If I saw something better.

If you invent a fusion reactor that can run a Tesla on a sugar cube for a 100 years and you asked me whether I would buy that instead of the [regular] Tesla — all things being equal — I think I like the car with the fusion motor or the atomic overthruster.

[But] I just haven't seen it. Bitcoin at its core is more of an ideology: let's implement conservation of energy in cyberspace via a protocol, which is fair and equitable. [Bitcoin has] done that.

I repeat: a fusion reactor that can run a Tesla on a sugar cube for 100 years.

Anyway, back to Saylor’s new analogies for MicroStrategy, which he calls the first “Bitcoin Treasury Company” in the world (the acronym is…BTC). This new version of MicroStrategy takes “raw Bitcoin” and “refines it” to offer a financial products that different parts of the market want to buy. He also compared this refinement process to electricity transformers in a recent conversation with Natalie Brunell:

[Our most] compelling business opportunity is as a Bitcoin Treasury Company. What we’re offering is securities backed by Bitcoin. The bond holders want low-risk Bitcoin. The equity holders want high performance Bitcoin. Some people want high-voltage Bitcoin. Some people want low-voltage Bitcoin.

The ETFs are offering raw [Bitcoin returns] and MicroStrategy stock was offering you 120 [volatility] and…levered high-voltage Bitcoin. [...]

So, in essence, MicroStrategy is like a big crypto transformer…Scary high voltage Bitcoin comes in the front and then on one side we step it up to be extreme high-voltage. That’s how you outperform Nvidia. You double Bitcoin or 1.5x Bitcoin.

And then we give everybody else low-voltage Bitcoin. Safe Bitcoin. Low-risk Bitcoin. Low-volatility Bitcoin on this side. The irony of it is everybody's getting exactly what they want. [..]

I have a 480-volt three-phase power on [my] dock. It'll power up a 500-ton yacht. You're not going to plug it into your blowdryer right?…I have a massive transformer to step down the power. There's a lot of value in giving people what they can consume and there's someone that makes a living converting that power into batteries and selling you little battery packs, so you can put it into your kid’s toys.

You know what the markup is [on converting power]? It's like a factor of a thousand markup.

Some investors want stocks. Some want government treasuries. Some want trading cards. Some want real estate. Some want corporate bonds. Some people want dick-shaped NFTs. Some people want Picassos.

One product MicroStrategy is offering that people want is Bitcoin-linked convertible bond notes. The main thing to know about this financial instrument is that an investor gets two components (Quant Bros has a fantastic chat on MicroStrategy’s entire convertible bond strategy):

A bond component: This is the debt portion with a coupon and a principal amount that is paid back at the maturity date (if the note doesn’t convert to equity).

An equity component: An embedded call option that allows the bondholder to convert the bond into equity at a pre-determined price (which is at a premium to the price of the stock when the convertible bond is issued).

The convertible bond market is worth ~$800B. It’s a fraction of the overall global bond market — which is ~$300T — but a pretty large pool of capital for MicroStrategy to tap.

Saylor dipped his toes into the convertible note pond with two issuances at the start of MicroStrategy’s Bitcoin journey:

December 2020: $650m at 0.75% interest (5-year term)

February 2021: $1.05B at 0.00% (6-year term)

In 2024, MicroStrategy has gone HAM with this product and offered five convertible notes and they have been oversubscribed, indicating high demand:

March 2024: $800m at 0.625% (6-year term)

March 2024: $604m at 0.875% (7-year term)

June 2024: $800m at 2.25% (8-year term)

September 2024: $1.01B at 0.625% (4-year term)

November 2024: $3B at 0.0% (5-year term)

In total, that’s ~$8B raised by selling convertible bond notes with funds allocated to buying more of that sweet sweet Bitcoin. These notes are due between 2025 and 2032 and may convert to MicroStrategy equity if MSTR hits the target stock prices.

The November 2024 convertible note of $3B has a 0% interest rate because investors are assigning enough value for the upside equity call option. Remember, MicroStrategy is very volatile because of how the equity component is tied to the change in the price of Bitcoin (which makes up 99% of the value of the company). If the convertible note doesn’t convert to equity, it’s a senior claim on the company’s assets (if MicroStrategy can’t pay back the debt).

Saylor currently has a major cost-of-capital advantage because there are huge swathes of the investment community — fixed income traders, hedge funds, corporate bond arbitrageurs, YOLO options maniacs — that want Bitcoin-linked debt and ability to trade Bitcoin-linked equity volatility. And MicroStrategy is really the only major player offering these products (well, there are also two absolutely bonker ETFs that are offering 2x leverage on top of MicroStrategy stock…very not investment advice).

MicroStrategy has also been able to raise funds by issuing shares of its stock (which is trading at a premium to the underlying Bitcoin…some may say its overvalued). While such equity issuances — and the conversion of its convertible debt into equity (if MSTR hits the right price) — will dilute the shareholders, many investors are fine with this outcome under the expectation that MicroStrategy will take the proceeds and buy Bitcoin. Presumably, that will increase the price of Bitcoin, which increases MicroStrategy’s holding of Bitcoin, which increases MicroStrategy’s valuation.

Some have noted that this capital raising and dilution strategy has a ponzi dynamic. But it’s completely out in the open. Also, MicroStrategy’s Bitcoin buys have so far been accretive. In laypeople terms: investors are seeing an increase in price per share even as their shares are diluted because the market is affording MSTR at least a 2x premium on its underlying Bitcoin (we will address whether or not this premium will hold in the next section).

Here are some quick bullet points to get us all on the same page:

MicroStrategy issues equity and convertible debt

It buys Bitcoin, which helps push the value of Bitcoin up

This increases the value of Bitcoin on MicroStrategy’s balance sheet

MicroStrategy issues more equity and convertible debt to buy more Bitcoin

This playbook is about to get wild.

MicroStrategy recently announced a plan to raise $42B — $21B in debt and $21B in equity — to buy Bitcoin. On its Q3 2024 earnings call, the company’s current CEO Phong Le (fellow Viet, whaddup?!) said that the total $42B capital raising target was a head nod to The Hitchhiker’s Guide To The Galaxy (the book’s protagonist finds out that the answer to the universe is the number 42). And, of course, “21” refers to “21 million” as in how much Bitcoin will ever be in existence.

I think this financial engineering dynamic partially explains the ~2x premium (and MSTR’s year-to-date gain of +465%). Another part of this premium has to do with the long-term prospects of Bitcoin and the meme-y association with Saylor, who has become one of Bitcoin’s greatest spokesperson.

So, what is the long-term play?

Saylor’s Long-Term Bet (and Risks)

I’m guessing right now that some of you have been screaming at your phone or laptop screen and asking “Trung, isn’t this entire MicroStrategy plan dependent on the price of Bitcoin continually going up?!!!?!?!?!?!?”

Absolutely.

There’s a running joke that Saylor found an “infinite money glitch” but there are limits to his strategy. However, Bitcoin doesn’t have to go up a ton to quasi-justify MicroStrategy’s plan.

The first thing to consider is that MicroStrategy has issued long-term debt. The shortest term is the 4-year ~$1B convertible note due in 2028. If Bitcoin tanks between now and then, the note wouldn’t convert to equity and MicroStrategy would be on the hook to pay it back (possibly having to liquidate some Bitcoin → which puts selling pressure on Bitcoin → which negatively impacts MicroStrategy’s Bitcoin holding → which hurts the stock price).

However, there has never been a 4-year period in Bitcoin’s history when it was worth less at the end as compared to the beginning of the period. Marty Bent writes that “Bitcoin’s lowest 4-year CAGR is 26% and its 50th percentile 4-year CAGR is 91%. If you think this will continue, then this is a pretty safe bet for MicroStrategy and the convertible note holders.”

Another thing to consider is that MicroStrategy will benefit from some technical changes in financial markets:

MicroStrategy’s potential inclusion in the NASDAQ or S&P 500 indices…which will lead to a wave of buying pressure from passive funds that need to match the index components.

A rule-change by the Financial Accounting Standards Board (FASB)…as of January 2025, public companies will be able to mark-to-market the value of its Bitcoin whether it goes up or down. Right now, MicroStrategy can only update its financial statements to reflect a Bitcoin decline but not a gain. If Bitcoin continues to run in 2025, MicroStrategy will report some wild earnings numbers based on the mark-to-market value of its Bitcoin investment, which will flow through the income statement. I’ve seen estimated Q1 2025 earnings in the $5-10B range (in the last quarter, MSTR’s software operating business lost ~$20m on sales of $116m). How will markets deal with these numbers? The traditional price-to-earnings (P/E) ratio seems inadequate (Saylor believes the long-term MSTR holders are most interested in Bitcoin per share as the key performance indicator (KPI) and is focussing on that number, which he’s dubbed “Bitcoin Yield”).

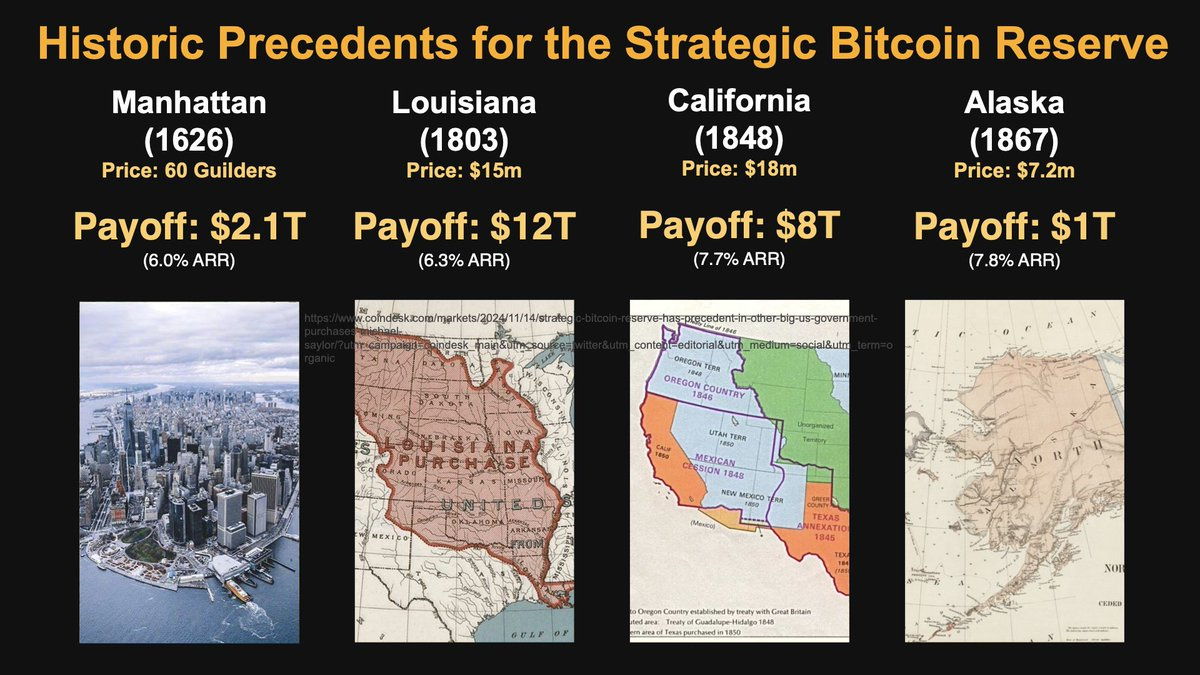

On the macro level, the incoming Trump administration looks very positive for Bitcoin and crypto. During his Presidential campaign, President-elect Trump mentioned the idea of a “Strategic Bitcoin Reserve” and — in a recent viral keynote for the Cantor Fitzgerald conference — Saylor explained why this is potentially a multi-trillion dollar opportunity comparable to the country’s largest historical land purchases (see slide below).

Here comes another analogy. Think through America’s most valuable land acquisitions (Louisiana, Manhattan, Alaska). Saylor calls Bitcoin the “Digital Manhattan” and there’s an opportunity to claim it because: 1) the supply of BTC is capped at 21,000,000; 2) the first rich country to announce its Bitcoin position will lead to a massive demand and price surge for the asset.

The appetite for non-dollar reserves has increased sharply. Central banks around the globe have cranked up the pace of Gold-buying for their reserves over the past 3 years. Part of it was in response to inflation and currency debasement. Part of it — especially in China — was in response to America freezing Russia’s US dollar-based Central Bank assets following its invasion of Ukraine in February 2022. Since then, the price of Gold has gone up ~44% from $1,800 to $2,600 (Goldman Sachs forecasts Gold to keep rising in 2025 as more emerging markets Central Banks buy the asset over “concern about the risk of financial sanctions”).

If Bitcoin can play a similar role as Gold as a store of value reserve asset, it won’t be long until a large economy announces that it “converted X% of its reserves into Bitcoin”. There’s major game theory here that is way above my brain capacity. All I know is that every country that comes after that first country, is at risk of paying a higher price.

The US Dollar is the world’s top reserve currency and the Fed has a target inflation rate of 2%. Something that costs $1 would cost $10 in 116 years (alternatively, you could say the purchasing power of the US Dollar decreased by 90%). That’s at 2%.

An investment in Bitcoin — a hard asset with a fixed supply of 21,000,000 coins — is one way to protect against this value destruction.

Gold’s market cap is worth about 10x more than Bitcoin right now ($17T vs. $1.9T). Broad Central Bank acceptance will close that gap (some napkin math: Bitcoin equalling Gold's market cap would make it ~$1,000,000 a BTC and Saylor's long-term price target — assuming a world in which everyone believes Bitcoin is the apex store of value — is $13,000,000...per...BTC...in 2045...and my calculator just broke calculating what MicroStrategy's current holding of 386,700 BTCs would be worth at that price level).

Granted, the idea of a “Strategic Bitcoin Reserve” may have already been priced in since Bitcoin has rallied ~40% since the election.

I do think that part of MicroStrategy’s premium to its Bitcoin holding is that the company is a well-oiled machine to buy up huge amounts of Bitcoin before rich nation-states step in.

Now, let’s look at some risks.

MicroStrategy has those ~$8B in convertible notes due over the next 8 years. Its Bitcoin is worth $37B+. Over this time frame, MicroStrategy is betting its premium to Bitcoin holds and Bitcoin gains somewhere at least 40-50%. If not, it might have to sell some of the Bitcoin holding, which could kick off a downward spiral (this scenario would probably require Bitcoin to fall to the $20-30k level and stay that way for many years).

The interest rates (<2%) are manageable and MicroStrategy will likely have options to roll the debt over with new debt. MicroStrategy also has such a strong brand in the crypto space that it could probably remake its software business into a crypto platform and create a valuable operating business on that front within the next decade.

To be sure, a long crypto bear market is certainly possible and MicroStrategy would take a major hit in such an environment.

Shorter term, many are betting against the premium that MicroStrategy stock has on its underlying Bitcoin. The number fluctuates but 15-20% of outstanding shares are held short (betting MSTR will decline).

As noted earlier, MicroStrategy is planning an additional $21B in convertible note issuances. If it completes that plan, the company would have $30B (or ~4%) of the entire convertible bond note market. Is that too much? Too little? How much appetite is there for this Bitcoin-linked convertible debt product? If it turns out there isn’t much more appetite, Saylor loses his cost-of-capital advantage and Bitcoin would have to probably 2x (to $200,000) to justify the existing valuation. At which point, why not just own the Bitcoin directly?

Crypto analyst Willy Woo laid out other reasons that MicroStrategy could lose its premium:

SEC: Do regulators step in on MSTR equity issuances?

Custodial Risk: It’s believed that MicroStrategy’s Bitcoin is held across Fidelity, Coinbase and other institutions (there are always risks with this type of arrangement).

Competition risk: Others publicly-traded companies could copy the Bitcoin treasury and convertible note issuance playbook. This would saturate the appetite for this type of product even faster (Coinbase already custodies a lot of Bitcoin and could credibly offer a Bitcoin-linked convertible note).

Assuming the above, what’s a worst-case scenario?

Geo Chen has a write-up on how the MicroStrategy’s Bitcoin buying operation could all unwind (“MicroStrategy will be reflexive on the way up and on the way down”):

At some point, the [MSTR] premium or BTC (or both) will stop going up and top out due to a mature crypto cycle and unsustainable blowoff top dynamics. At that point, MSTR's most recent convertible note issuance, which likely will have been the biggest it has done so far, will fail to reach its conversion price, resulting in the issuance remaining as debt (and therefore leverage) instead of share issuance. Perhaps Saylor will attempt to issue more convertible debt as the market is in the process of topping in an attempt to support the market and his stock price. This will result in him piling on even more leverage at the top of the market while pulling his BTC cost basis even higher.

The market will eventually catch on to how precarious this is, and start closing the premium at the same time BTC is likely topping out. The most recent shares that converted at the high will be the first to panic sell. There are also 2x leveraged ETFs on MSTR with several billion in AUM that add more leverage to the MSTR system. As the premium closes, MSTR's ability to issue more shares will be impaired as reflexivity works against them. At some point the sell pressure may potentially push MSTR's premium to a discount to their NAV as the market smells blood in the water. Some in the market will see this as a bargain, but this will actually be a value trap as the market will be selling both MSTR and BTC to force them to capitulate sell to raise cash to fund their debt. The threat of MSTR having to sell their massive holdings of BTC will be enough to trigger the next crypto winter.

Again, none of this is investment advice. I’m not touching the MSTR trade with a thousand-foot pole because I just can’t stomach the volatility. But it is one of the more fascinating stories in the markets right now and I am positive the memes will be incredible however it shakes out.

This issue is brought to you by Bearly AI

Why are you seeing this ad?

Because yesterday was Black Friday and I’m obligated to plug a product in this newsletter.

On that note, I co-founded an AI-powered research app called Bearly AI that can save you and your team hours of work with AI-powered tools for reading (instant summaries), writing (GPT-4o, Claude Opus 200K, Grok, Gemini) and speech-to-text transcription tools (Scribe, Whisper).

It’s all available in one keyboard shortcut (and an iPhone app). Use code BEARLY1 for a FREE month of the Pro Plan.

Links and Memes

Apple TV+’s weird $20B+ strategy: Apple set off a row last week when it released the film Wolfs — starring really good-looking older dudes (Brad Pitt, George Clooney) — directly onto its streaming service…after previously promising a theatrical release. Wolfs has turned into Apple TV+’s top-streaming film ever but director Jon Watts said he cancelled a sequel because he “no longer trusted [Apple] as a creative partner”.

Apple’s strategy here makes no sense. They’ve already spent money to produce the film and are swimming in cash. Who cares if it flops in theatres. Don’t piss off the creative talent when you’ve already made the investment.

This Wolfs story is the latest example of Apple splurging 98% of the way through a creative project but then stopping short of the finish line.

Per Bloomberg, Apple TV+ has spent $20B+ on original films and TV show. Despite the splurge, the streaming service “generates less viewing in one month than Netflix does in one day” and accounts for only 0.2% of TV viewing in the US (vs. 8% for Netflix). One reason for the disconnect is its lacklustre marketing efforts relative to the quality of content including TV shows (Severance, Slow Horses, Pachinko, Disclaimer, Ted Lasso) and films (Tetris, Killers of the Flower Moon, Coda).

When you think of HBO, you think premium. That’s not top of mind with Apple TV+ even though it has a good track record. It’s not top of mind because I don’t even know what Apple TV+’s brand is supposed to be. Back in the mid-2010s, there were actually rumors of Apple acquiring HBO (AT&T ended up buying the company in 2016). That would have been cheaper than $20B+ — maybe half the amount — and Apple would have gotten a back catalog and the brand reputation that it hasn’t been able to build.

Now, Apple wants to rein in costs based on the “Apple Tax”, the idea that the $3T iPhone maker will pay a huge premium to make content simply because its loaded. It’s done so for shows such as The Morning Show and Severance. And really gone all out for top directors like Martin Scorsese and the $200m+ budget for Killers of the Flower Moon. This all helps to explain the Wolfs decision but still kinda weird.

PS. If you know how I can get some Apple Tax in my life, please reply to this e-mail.

***

My Gladiator II Review: Speaking of theatrical releases, I went to watch Gladiator II last Sunday. As with my theatre visit to watch 85-year old Francis Ford Coppola’s Megalopolis, I felt obligated to pay tribute to 86-year old Ridley Scott and 69-year old Denzel Washington.

Ugh, it was so bad, though.

A microcosm for the film was when they filled the Colosseum with water for a sea battle. These Colosseum sea battles actually happened in Ancient Rome but Scott decided to put sharks in the water. Sharks, people, sharks.

When asked about the historical accuracy of sharks in the Colosseum, Scott snapped during a Collider interview:

“Dude, if you can build a Colosseum, you can flood it with fucking water. Are you joking? And to get a couple of sharks in a net from the sea, are you kidding? Of course they can.”

Well, that settles it.

The “sharks in Colosseum” is almost too on the nose for Scott “jumping the shark” in the sequel. Nominally, the plot is set ~20 years after the original Gladiator starring Russell Crowe as Maximus and Joaquin Phoenix as the villainous Commodus. But the entire film feels like a vehicle to shoehorn favourite lines for the sake of nostalgia (“What we do in life, echoes in eternity”, “strength and honor”).

It’s pretty much a beat-by-beat remake with Paul Mescal in the lead role (and Denzel playing a prominent villain role). The only change is the beats have something crazier than last time. Like a shark. Or fighting monkeys and giant rhinos. There are some great visuals (riots, large Roman armies) but none of the sequences feel earned. Everything is rushed. There’s very little character development. And all the “reveals” are super predictable. It’s way too long at 2.5 hours. Can’t believe this thing cost $250m.

Denzel was solid, though. So if you a ‘Zel fan, hit it (or just watch this really good TikTok of someone pretending to be Alonzo from Training Day pretending to be Macrinus in Gladiator II).

In sum: the first Gladiator — especially with the Hans Zimmer soundtrack — was kind of perfect…and we did not need a sequel.

WATCH MORE: Discovery UK has an 8-minute explainer on how Roman engineers filled the Colosseum with water. Nerdstalgic has a baller 9-minute on how Gladiator won Best Picture without a script.

***

Why Dermatology is Surging: I’ve had a number of doctor friends tell me over the years that they regret not doing dermatology.

Compared to a lot of other specialties, dermatologists have a more predictable schedule (35-40 hour workweeks are the norm), fewer late-night calls, less admin and potential for higher pay.

Te-Ping Chen at the Wall Street Journal recently wrote about dermatology and how it turned into one of the most competitive specialties, with student applications up 50% over the past 5 years.

In addition to a high median salary ($541k vs. $258k for paediatrician), many dermatologists are taking advantage of booming interest in skincare by building large social followings on TikTok and Instagram. From there, they supplement their income by hawking skincare products and cosmetic treatments such as micro-needling, injections and laser therapy.

It’s a sea-change for the field. In the latter half of the 20th century, Chen writes that dermatologists were noted for treating venereal diseases and the skin lesions for HIV patients. This culminated in a joke on Seinfeld when Jerry called a dermatologist he was dating “Pimple Popper, MD”.

But then the FDA cleared Botox for cosmetic treatment in 2002. The specialty started taking off as Hollywood went deep on the product. Dermatologists also saw their visibility rise with increased awareness of skin cancer, the most common cancer in the US.

When I posted this story on socials, other doctors chimed in with some additional color. Many agreed that dermatology is a great work-life-balance but also thought the speciality was boring relative to other specialties (and maybe not intellectual stimulating enough for a decades-long career). I have zero insight on whether or not that's correct but felt it was worth sharing.

One additional thing I want to flag about this article.

My wife was telling me over a decade ago about how the dermatology field was primed to grow. Her perspective came from someone that is really into skincare and — and as a consumer — realized how many add-on products there are and how it was relatively low-stress (compared to a surgeon or ER doctor etc). Reading this article was just a reminder that women control 75% of consumer discretionary spending and that my view on countless industries is functionally useless since I live in such a weird bubble of doomscrolling internet memes and listening to history podcasts that don’t actually make contact with consumer reality.

Read More: The recent Ozempic craze — that has led to the thinning of America — has also trickled down to the beautification industry. According to The Hollywood Reporter, there is currently a “De-Kardashian-ification” of beauty standards that is “deflating boobs, shrinking butts and [making] little lips”.

…and them fire posts:

Just when we thought the Drake vs. Kendrick beef was over, it’s very not over. First, Kendrick released a new album and a wave of “don’t let Drake see this” memes came out. Second, Drake hit Kendrick’s record label Universal Music Group (UMG) with two lawsuits in the past week.

One lawsuit charged that the label used bots to artificially boost streams of Kendrick’s brutal diss song “Not Like Us” to crowd out other songs and make it look bigger than it actually was. The second lawsuit charged UMG with defamation since Kendrick’s song included lyrics suggesting that Drake is a sex offender. None of these allegations in either direction have been proven in court. Drake’s lawyers even pulled out the RICO act — typically used against organized crime — to allege that UMG was trying to ruin his career. One theory is that UMG wants to de-value Drake’s catalogue — worth $400-500m — ahead of new negotiations with the artist on future payouts. Total speculation. Either way, Kendrick won but I still rock Drake tracks and the court of public opinion seems to think Drake is on sour grapes.

We watched it last night and thought of the shark jump! Really how are they going to get sharks there, just go with it I guess.

Dermatology sounds like it's closer to plastic surgeons that medicine which also pays much better than helping people that are sick, at least there isn't a shortage of doctors...

I like your wife!