Spirit Airlines & The Airplane Boneyard

The business model behind storing, converting and disassembling airplanes.

Thanks for subscribing to SatPost.

Today, we will talk about all things airline industry including Spirit Airlines shutting down, Delta’s absurd credit card business and what happens to retired planes.

Also this week:

Nvidia’s $3B Deal With Glassmaker Corning

RIP Ted Turner

…and them wild posts (including the Met Gala)

Spirit Airlines shut down last Saturday after a failed attempt by the US government to bail out the 34-year-old budget carrier.

We’ll discuss more on how the business collapsed in the next section.

But first let’s cover a less consumer-facing part of the airline industry: the business of storing, refurbishing, converting and dismantling planes.

Spirit Airlines’ employee count has shrunk from 17,000 to less than 100, and most of the remaining executives are figuring out what to do with the company’s fleet of Airbus planes.

For some reason, Spirit didn’t do the most obvious solution:

Instead, here is the state of the fleet per USA Today:

According to data from Cirium, an aviation analytics company, Spirit had 172 planes in its fleet when it shut down on May 2. Of those, 95 were in active service and 77 were in storage, largely in Arizona. A majority of Spirit’s planes (124) were leased, which means they’ll automatically be returned to the lessor.

Some of the 48 owned planes were also signed over to a lessor previously, meaning the bankruptcy proceedings will only result in a direct sale of a few of the aircraft in Spirit’s fleet.

Many of those active planes flew to Arizona in the days since Spirit closed shop.

Why? Arizona’s desert climate makes it a go-to spot for what is known as airplane boneyards.

“The sun shines for some 300 days a year,” explains The Economist. “Humidity levels hover in the low double digits. It is so dry that the soil, known as caliche, hardens to a cement-like consistency—ideal conditions for storing planes, heavy things whose enemy is corrosion-causing moisture.”

Arizona has about 4,000 airplanes stored at various sites including the military-focussed Davis-Monthan United States Air Force Base (which you may or may not have seen in Transformers) and the commercial-focussed Pinal Airpark (which you may or may not see in this photo below).

Other major plane storage areas are located in similar climates including Southern California (Victorville, Mojave Port), New Mexico (Roswell International Air Center), Spain (Teruel Airport) and Australia (Alice Springs).

The Economist provides more detail on how the Arizona airplane boneyard ecosystem works and it’s fascinating:

Storage: It costs $5,000 a month to park a single-aisle plane or $10k for larger jets. Some of you space-strapped NY or SF readers are probably running the math to see if it makes sense to just live in Pinal Air Park and work remotely.

Disassembly: A large jet (e.g. Boeing 777) has over 130k unique parts (~3m total) including bolts and rivets. Airlines need a “reliable supply of all these bits and pieces” or the “global aviation industry would grind to a halt without them”. All parts have to be certified and need a comprehensive maintenance history to retain value.

Parts Resale: Cockpit instruments “can be removed and reused in other aircraft of the same type” and “sometimes the entire cockpit is repurposed as a simulator for pilot training”. Avionics, instruments, wiring and hydraulics are sold or stored based on demand. Luxury seats at the front of planes are re-sold to 2nd and 3rd tier airlines or aviation collectors.

As with real life, the “least desirable” parts of the plane are the economy seats. These are made with 20-30 different materials and shredded for waste. Some airlines try to limit the waste by using higher-end material (e.g. Emirates has 14 tailors to “repurpose materials from its cabins into bags, wallets and suitcases, with proceeds from sales going to charity”).Refurbish or convert: Older planes on the brink of retirement are able to stay in the air if smaller carriers — particularly from developing markets — buy them up and update parts. Richer airlines “prefer factory-fresh aircraft because of fuel efficiency and customer expectations”.

Another common way for old commercial planes to stay in the air is for them to get converted to cargo planes. This adds 10-20 years because “despite higher operating costs, second-hand planes offer better value to logistics firms than more efficient but pricey new ones because freighters clock fewer hours in the air than passenger services.”

The Spirit Airlines fleet is mostly spoken for but the ones that do go on sale will probably end up with other low-cost carriers…which means we won’t get to see this Project Hail Mary.

Why The Airline Business Sucks (and How Delta Is Making It Work)

David Oks wrote a very insightful piece on why the airline industry is so prone to bankruptcies.

The statistics are actually jarring:

“From its deregulation in 1978 to the end of 2025, the airline industry has cumulatively lost money: its net profit over those 47 years sits at negative $37 billion.”

“Between 1978 and 2005, more than 160 airlines filed for bankruptcy.”

“In September 2005, every one of the four largest American airlines—United, Delta, Northwest, and US Airways—was operating simultaneously under Chapter 11 protection.”

Warren Buffett has gotten burned by many airline stocks.

Probably (but also maybe not) in jest, wrote in his 2007 annual letter that: “A durable competitive advantage [in the airline industry has] proven elusive ever since the days of the Wright Brothers…indeed, if a farsighted capitalist had been present at Kitty Hawk, he would have done his successors a huge favour by shooting Orville down.”

So, what gives?

Oks gets deep into game theory and a key part that stood out was how huge fixed costs and volatile cyclical demand entices new entrants before flushing them back out:

Suppose you’re managing an airline that does flights from San Francisco to Tokyo. (A flight I’m considering taking, by the way.) Most of your costs, you’ll find, are fixed. The aircraft itself — let’s say it’s a modern widebody, like a Boeing 787 — will cost you somewhere in the low hundreds of millions; that’s a fixed cost. So are the gate slot for your departure from San Francisco and the landing rights for your arrival in Tokyo.

Labor costs might seem variable, but they’re actually not: pilot, flight attendant, and mechanic compensation in the United States is governed by the Railway Labor Act of 1926 (which was extended to airlines in 1936), which stipulates that collective bargaining agreements don’t actually expire but rather remain in force until they’re replaced. So even your wage bill is more or less fixed over multi-year horizons. The most variable major cost you’ll have to deal with is jet fuel; but given that spiking fuel prices aren’t your friend, you’d rather hedge fuel costs aggressively to smooth out cash flow. So fuel also acts more like a fixed cost.

All of which is to say: you have a lot of fixed costs.

Now let’s suppose daily demand on your route from San Francisco to Tokyo is roughly 800 passengers willing to pay a price that covers the full cost of flying. A widebody seats around 250 to 300 people. Perhaps you offer one flight per day, and you have two competitors that also offer one flight a day. This puts about 750 to 900 seats into the market: close enough to demand that fares stay healthy and the route covers its costs, plus a bit extra that you and your competitors can take as profit. Some customers don’t fly, and fares get bid up; but this is fine enough, at least for you.

But there’s a problem with this situation: there’s enough slack in the market —enough customers paying more than they could, and enough margin that you’re taking — that a new entrant could see an opportunity to enter. And once that new competitor has entered, you now have 1,000 to 1,200 seats chasing 800 passengers, which means that somebody has to lose out. The efficient number of daily flights is somewhere between three and four; but capacity is lumpy. So whereas three was somewhat too few, four is definitely too many. So you enter the instability part of the cycle. Fares collapse; margins take a hit; eventually someone has to exit. Once the weakest competitor has exited, the market consolidates again, and fares recover; but then someone sees the unmet demand and enters again.

So even in the best of times, there’s a deep structural instability to the airline industry: margins are structurally depressed and companies are unable to recoup their cost of capital. And that is in the best of times.

Because of this dynamic, a 100% competitive free market leads to repeated failures and airlines frequently operate while in Chapter 11 bankruptcy protection in an effort to reduce these fixed costs (e.g. union negotiations).

While Spirit was profitable in the 2010s, the broader airline industry has very much not been in the best of times since COVID.

Spirit Airlines tried to merge with JetBlue in 2024 but that deal was blocked by the US government on anti-competitive grounds. The reality was that 80% of the US airline market is controlled by 4 companies (United, Delta, Southwest, American Airlines).

A JetBlue tie-up with Spirit Airlines would have allowed the combined entity to better manage the industry volatility…including the spiking fuel prices since the start of the Iran conflict.

But we know what happened.

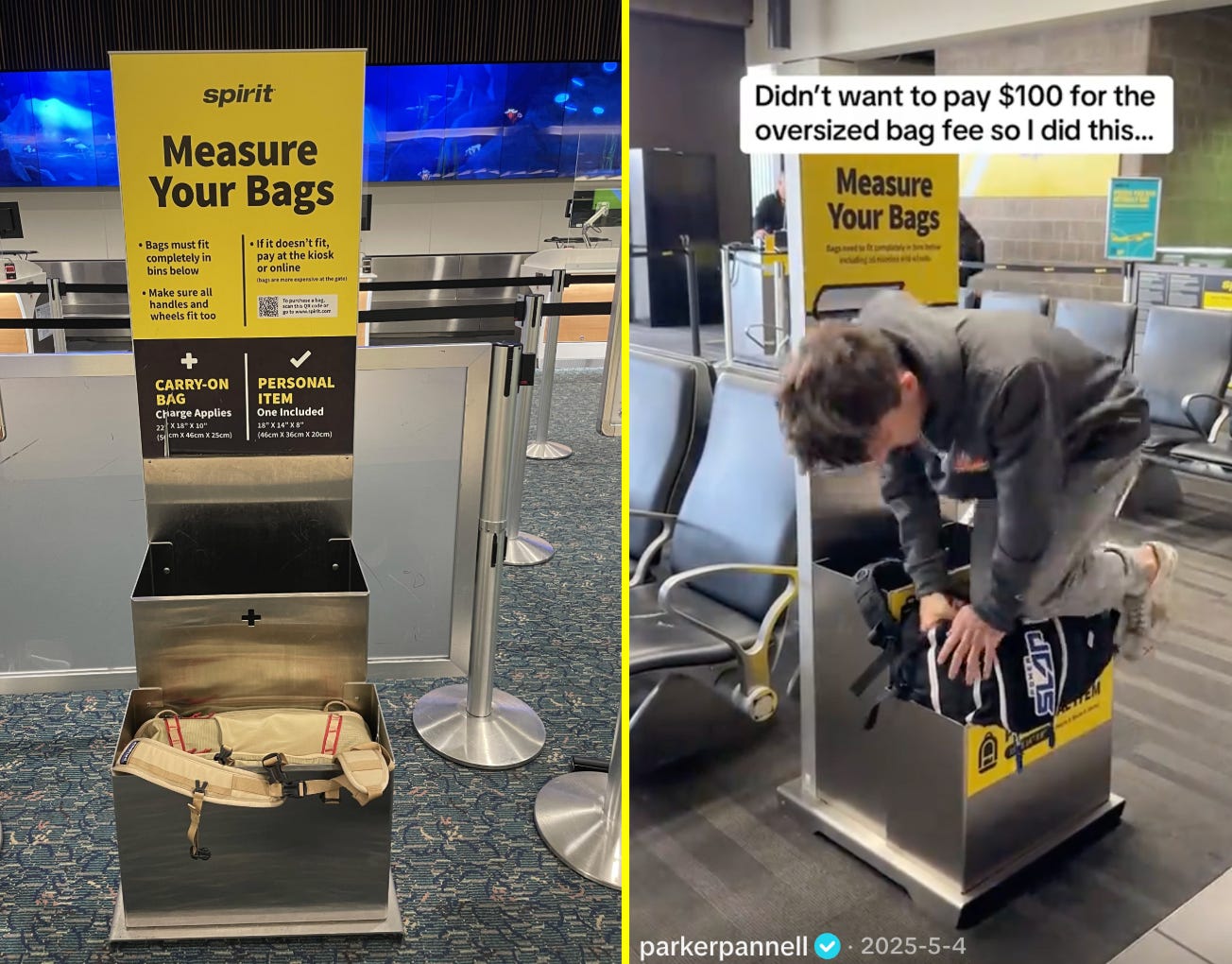

It’s unfortunate because Spirit — and other budget carriers — do keep the major airlines on their toes. In 2010, Spirit became the first domestic airline to charge for luggage. The aggressive unbundling of the flying experience allowed them to cut tickets to the bone. It also made Spirit one of the most aggressive monitors of those baggage sizer things at the gate…they were on you like white on rice if your laptop backpack was too big.

That’s how we got $25 one-way flights from Atlanta to Fort Lauderdale, which was Spirit’s HQ.

Per WSJ, Spirit had 5% of the domestic air travel market in 2023 but fell to 1.8% in 2026…and when it exited a route, the ticket price increased by 23%. Expect some ticket prices to go up.

The way to make airlines work in America has been to avoid a perfectly competitive market (internationally, the most baller national carriers get ALOT of government support e.g. Singapore Airlines, Qatar Airways, Emirates, Turkish Airlines etc.).

This explains why airlines team up in “alliances” (Star, SkyTeam, Oneworld). They do codeshares and scheduling to limit competition. Another way is the hub-and-spoke model. The Big 4 Airlines funnel flights through key differentiated hubs and basically have regional monopolies:

Delta (market cap = $47B): Main hub is in Atlanta (followed by Detroit, Minneapolis, Salt Lake City)

United Airlines ($30B): Main hub is in Chicago (followed by Denver, Houston, San Francisco)

Southwest Airlines ($19B): Main hub is Denver (followed by Chicago, Baltimore, Dallas)

American Airlines ($9B): Main hub is Dallas-Fort Worth (followed by Charlotte, Miami, Philadelphia)

New budget airlines often enter by trying to monopolize secondary airports (basically how Ryanair dominated Europe) or certain routes (eg. Allegiant Air and all things Las Vegas).

But the real way airlines in America try to make the business of airlines work is to not be in the business of airlines at all. Just as McDonald’s is a real estate company disguised as a fast food company, the Big 4 airlines are credit card loyalty programs disguised as winged transportation.

In 2024, the four largest airlines in America made a combined operating profit of $14B. Per The Economist, the profit was almost entirely from credit card issuers paying airlines for points (every airline operated its passenger business at a loss):

Amex paid $1.2B to Delta Airlines (the airline’s entire operating profit for the year)

Citigroup paid $1.4B to American Airlines.

JPMorgan paid $800m to United Airlines.

Incredibly, ~1% of US GDP is spent on Delta-branded Amex credit cards (Amex paying for those juicy juicy business travellers...let's just say there was never a Spirit Airlines Amex card).

All of these airline loyalty programs are floated by the ~2% credit card interchange fees paid by merchants, reaching a total of $160B a year (on a $100 transaction, the credit card issuer takes $2 and typically gives $1.50 as reward/rebate/points back to the customer while keeping the remainder).

In the past 8 years, Delta and American doubled revenue from selling airline points. When the airlines were shut down during COVID, the value of the points program was worth more than the actual flying operation…and the airlines borrowed money with the loyalty programs as collateral.

The budget carriers forced the Big 4 to create the comically narrow seats Basic Economy price option and they’ll continue to float it because of the credit card cash machine (in other words, prices may actually not rise that with Spirit gone).

One caveat: anyone that has recently been to an airport lounge knows that these credit card programs are hitting the limits. The Centurion Lounge doesn’t feel so lounge-y when there is a 27-person line wait for the pesto pasta in the salad bar (which does slap).

Delta has taken the “do non-airline stuff” to another level. In 2012, it bought a Pennsylvania-based refinery from ConocoPhillips for $150m and another spent $100m to upgrading it. Its subsidiary is called Monroe Energy and it refines 200,000 barrels a day. Half of the barrels are refined into jet fuel and the rest is gas and diesel, which Monroe then sells on the market or trades for more jet fuel. Overall, the operation supplies 75%+ of Delta’s domestic fuel needs.

Every other airline and most energy expert laughed in Delta’s face when they made the move. While the logic is straightforward (fuel is 20-30% of an airline’s operating cost), owning a refinery is so far outside of an airline’s circle of competency.

The airline industry was content to hedge fuel prices to manage volatility, but that practice mostly stopped by the start of 2026. Why? Airlines decided it was easier to pass any price increases onto customers as a fuel surcharge.

Delta was able to make back its investment within 5 years but it has now spent $1B+ in maintenance and the operation is still very cyclical.

During COVID, the refinery lost $140m in Q2 2020 and Delta considered selling the operation. When the Ukraine-Russia war began in 2022, Monroe saved Delta a lot in fuel costs as oil prices jumped. Then, in 2025, the refinery business hit $5B of sales in 2025 (~8% of Delta’s total) and saved the airline 4 cents a gallon on jet fuel compared to the market (~$100m cost savings). Due to the current Iran conflict, it is expected to see a $300m earnings gain in Q2 2026 as the “crack spread” (price difference between oil vs. refined products) is at all-time highs.

So, yeah, Delta is showing that the most profitable way to run an airline business in America is really to not be in the airline business. No guarantee it’ll save them from future bankruptcy (unless it pivots to AI data centres).

***

Here are some other relevant airline links:

The pilot announcement from one of the final Spirit Airlines flights…might put you in the feels.

Another Spirit Airlines pilot was supposed to do his retirement flight on Saturday…but the airline shut down before he could. He boarded a Southwest Airlines plane to head home and the flight’s crew found out. When he arrived in Baltimore, the Southwest staff waited for him at the gate, gave a bottle of champagne, then let him do a water-cannon salute in a Southwest plane.

Speaking of Southwest Airlines, its legendary founder Herb Kelleher…once got into a trademark dispute. Back in 1992, Southwest Airlines had the motto “Just Plane Smart”. Another aviation firm had the motto “Plane Smart”. The beef was resolved with an arm-wrestling match between the CEOs. It was dubbed “Malice In Dallas” and held at a 4,500-seat wrestling venue. Despite smoking a cigarette, legendary Southwest CEO Herb Kelleher somehow lost to Steven Aviation’s Kurt Herwald. In the end, Southwest kept its slogan in exchange for a $5k charity donation.

Honestly, Spirit Airlines CEO should have gotten a chance to arm wrestle the airline’s creditors to save the business.

Finally, here are some related posts:

This issue of SatPost is brought to you by OpenADE

Do you want to get the most out of Codex and Claude Code?

Then try OpenADE, a free open-source tool to maximize AI coding with better planning and collaboration features.

Most AI coding tools throw agents at your codebase and hope for the best. You end up babysitting, fixing hallucinations, and wondering if the “AI-assisted” code is actually worse than writing it yourself.

OpenADE takes a different approach: Plan → Collaborate → Revise → Execute.

The Bearly AI team built this tool internally and it is now 90% of our screen time, replacing our IDE and terminal.

By spending time upfront to craft and refine your implementation plan, you can run agents linearly with confidence. No more context-switching. No more “wait, what did it just do?” moments. Just saturated throughput and maximal work done.

Nvidia’s $3B Deal With Glassmaker Corning

My favourite iPhone launch story is when Steve Jobs dug deep in his reality-distortion field bag of tricks to convince the CEO of glassmaker Corning to commercialize Gorilla Glass.

In his book “The One Device”, Brian Merchant gives a play-by-play:

Jobs told [Corning CEO Wendell] Weeks he doubted Gorilla Glass was good enough, and began explaining to the CEO of the nation’s top glass company how glass was made.

“Can you shut up,” Weeks interrupted him, “and let me teach you some science?”

Jobs was sold, and, recovering his Jobsian flair, ordered as much as Corning could make — in a matter of months. “We don’t have the capacity,” Weeks replied. “None of our plants make the glass now.” He protested that it would be impossible to get the order scaled up in time.

“Don’t be afraid,” Jobs replied. “Get your mind around it. You can do it.”

According to [Walter Isaacson’s biography on Jobs], Weeks shook his head in astonishment as he recounted the story. “We did it in under six months,” he said. “We produced a glass that had never been made.”

The speed with which Jobs was taught science then incepted Weeks is unreal.

Anyway, I bring this up because Corning recently struck a new deal with Nvidia which may be just as transformative.

The 176-year old Corning has ridden various waves as the world’s top glassmaker.

Through most of the 20th century, it was known for its heat-resistant kitchenware (e.g. Pyrex). During the Dotcom/Telecom Bubble, its fiber optics were in demand. Then, it rode the mobile revolution after Jobs distorted Wendell Weeks’ reality field.

Now, it’s the AI wave. Earlier this year, Meta agreed to a $6B deal to lock down Corning’s fiber optic cables for its data centres. Nvidia just agreed to invest up to $3.2B into the company and Corning will build three factories in North Carolina and Texas specifically for Nvidia products.

The plan is to replace the >2 miles of copper inside of every Nvidia GPU server rack with something called co-packaged optics. Why? According to Weeks, moving photons (via optics) requires 5-20x less energy than moving electrons (via copper). Optics also provide much lower latency to produce tokens.

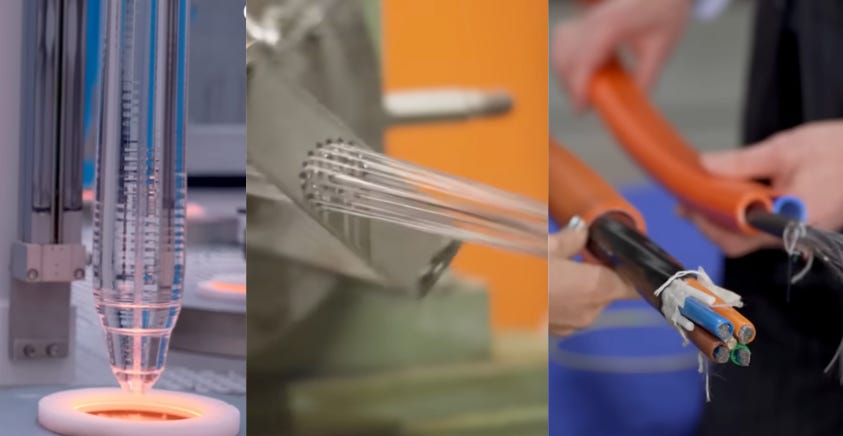

CNBC has a solid explainer video on the manufacturing process for Corning’s fiber optics:

a combustion process deposits glass soot on the outside of a rod

a machine applies extreme heat until the glass is clear and remove any impurities because impurities lead to signal loss (crazy fact: if the Indian Ocean was covered by this glass, you could see all the way to the bottom)

another machine draws the glass fiber until it’s hair thin (125 microns in diameter)

Corning then applies coating and color codes the material (for end buyers to identify use cases)

the fiber is then wind onto spools (one spool can go as far as 31 miles)

last step is to bind a bunch of fibers (up to 288 different ones) together and add a protective outer jacket

In 2025, optical communication was Corning’s largest division, accounting for 40% of its $16B in revenue (overtaking the glass business for smartphones and TV in the past few years).

Corning’s market cap has tripled in the past year from $50B to $150B. Wild.

RIP Ted Turner

The media mogul behind died at age 87.

Super interesting career. Turned his family’s outdoor advertising business into a cable TV empire anchored by TBS and TNT. Was also a star sailor who won the America’s Cup in 1977. Turned love of sports into the ownership of Atlanta Braves and Atlanta Hawks. Used those assets to fill up countless hours of TV time. In 1980, he launched CNN and pioneered the 24/7 news model. Then, launched WCW Wrestling, Cartoon Network and Turner Classic Movies (after spending $1B+ on MGM’s film library).

Live sports and around-the-clock news is still with us today for better and worse (CNN really surged in late-1980s and early-1990s for its coverage of the fall of the Soviet Union and the First Gulf War).

Turner had a lot of demons, was very outspoken and held contradictory opinions on everything. The absolute best long-read on his life is this 2001 New Yorker piece titled The Lost Tycoon. It was written following his divorce from Jane Fonda and Time Warner’s disastrous $150B merger with AOL, which pushed him out of his companies (Time Warner had acquired Turner’s networks in 1996).

One of Turner’s favourite quips was “"Early to bed, early to rise, work like hell and advertise"…and the New Yorker article has a perfect anecdote for that motto:

In November of 1996, for instance, the Friars Foundation honored Turner at a lifetime-achievement black-tie dinner. After he received his award and made a short speech, the lights dimmed, and then, as various entertainers, including the comedian Alan King, prepared to roast him, Turner, who insists on getting to bed early, grabbed Fonda’s arm and departed, leaving the crowd gasping and King bellowing, “Rupert Murdoch was right—you are nuts.”

Turner spent final decades of his life focussed on environmental, conservation and humanitary work (although, he was very wrong about the threat of overpopulation).

My favourite random Turner nugget is how he is prob most responsible for the wild popularity of The Shawshank Redemption (still #1 rated IMDB film).

In 1993, he buys Castle Rock and gets the film rights to Stephen King’s novel. The film flops in 1994. For the record, it’s an incredible flick but just not super commercial. It was also part of the great “Best Picture nominee” class ever along with Forrest Gump, Pulp Fiction, Four Wedding & a Funeral and The Quiz Show.

But then it went HAM on cable TV.

Director Frank Darabont said, “Turner started airing [it] on TV like every five minutes for years. There was this endless opportunity for people to catch up with it on a Turner network, and so I bless Ted Turner as well. Because he played the heck out of it."

The Shawshank Redemption only made $16m box office in first run but hundreds of million in second life as VHS, DVD and licensing.

As Bill Simmons would say, one of the ultimate films where no matter which part of the film you stumble on, you’ll want to finish the rest of it.

Among most shown films on cable ever (need to fill that airtime) and I probably watched it 25x to 35x because of Turner.

One last amazing detail: Stephen King never cashed the $5,000 check he got for film rights. King framed it and sent it to Darabont with a note: “In case you ever need bail money. Love, Steve."

Anyway, TNT had a solid video tribute before recent NBA and NHL playoff games…and here are some related posts:

Links and Memes

The economics of thoroughbred horse breeding: Last weekend, Golden Tempo won the Kentucky Derby in an amazing sprint from last place. The $3.1m winning purse is split with 10% to the jockey ($310,000), 10% to the trainer ($310,000) and 80% to the owner ($2.48 million). But the most interesting part business angle is that Golden Tempo is now highly in demand as a mating partner and could be worth $25 million to the owner, as explained by Joe Pompliano:

The economics are driven by pedigree: winning major races like the Kentucky Derby or producing champion offspring can dramatically increase a stallion’s fee and lifetime earning potential. Top stallions then breed 100–200 times per year, turning a single elite horse into a multi-million-dollar annual revenue stream.

The entire multi-billion-dollar breeding economy rests on a single rule enforced by the Jockey Club, horse racing’s North American registry. This rule states that every thoroughbred must be conceived through “live cover,” a witnessed natural mating between a stallion and a mare. Or, in other words, artificial insemination, embryo transfer, and cloning are all explicitly banned, which effectively caps supply and supports the premium pricing that makes a $250,000 stud fee possible.

This is straight econ 101. Just as Louis Vuitton controls the supply of its luxury products by monitoring inventory and going after fakes…horse breeders have to do the same, including paying someone to “live cover” — aka watching horses bone — to maximize value.

***

Some other links for your weekend:

“How Istanbul Won the Mobile Puzzle Wars”: Great episode of GameCraft podcast explaining how Turkey is a world leader in mobile games. Part of it is talent. Part is the government directly supporting the industry. Part of it is talent arbitrage…local developers paid in inflationary Turkish Lira while games mostly bring in USD and EUR.

10% of AMC movie showings sell no ticket… and someone created a site to find these showings so you can “go enjoy your private theater”.

Greg Abel had Warren Buffett speak at start of the 2026 Berkshire Hathaway AGM…Buffett spent most of it praising Tim Cook, seated a few rows behind next to John Ternus. Since 2016, Berkshire’s $35B initial investment officially grew to $185B.

If EU built ChatGPT…it would almost certainly look like this.

An X thread of what websites used to be…including OpenAI (a homepage for a guy named Glen), OnlyFans (a music site) and you will never guess in a million years what DoorDash used to be.

Anthropic is buying compute from xAI…this comes a few weeks after xAI (really, SpaceX) agreed to acquire AI coding startup Cursor. Basically, Elon went all-in on building compute but Grok isn’t using up the capacity. But there is such a shortage of chips that he’s been able to leverage xAI’s massive Memphis data centres for other companies desperate for compute (really, Anthropic). Makes sense on both sides. Claude gets to increase capacity while SpaceX’s upcoming IPO can report a ballpark ~$6B compute business from its AI arm (compared to only $500m from Grok itself).

The Odyssey trailer…man I hope Nolan doesn’t flub this.

The iPhone Fold (aka Ultra) is coming…and Unbox Therapy has a solid hands-on breakdown of the form factor based on leaks.

GameStop is trying to buy eBay. One problem is that GameStop is a $10B company while eBay is $50B. GameStop CEO Ryan Cohen went on CNBC and said the deal was “1/2 stock, 1/2 cash”. Asked to clarify, he repeated “1/2 stock, 1/2 cash” and that’s it. Problem is that GameStop only has $9B cash and one bank has apparently agreed to extend $20B in debt. That leaves $25-30B. GameStop isn’t allowed to issue that many shares and stock would collapse if it did.

Anyway, I’m telling you all this because as part of his campaign, Cohen listed items on eBay (used socks, a sealed box of Windows Server 2000) to “help” finance the deal then he proceeded to say that eBay suspended his account…then internet sleuths realized it wasn’t suspended. Incredible content…and it’s all happening because Cohen’s incentive package includes a massive amount of stock if he can make GameStop worth $100B.

…and them wild posts (including Sam Altman texts to former OpenAI CTO Mira Murati the weekend he got fired came out during Elon’s lawsuit against OpenAI...and, ugh, someone turned the exchange into a Hamilton musical):