6 Takeaways From Citrini's Viral AI Doomer Article (and a Bunch of Rebuttals)

Can an AI productivity boom tank the economy? Maybe. Maybe not. Buy maybe. But, also, maybe not.

Thanks for subscribing to SatPot.

Today, we have to talk about Citrini Research’s uber viral AI doomer report (and a lot of rebuttals).

Also this week:

Norway’s Sporting Secret Sauce

Paramount Outbids Netflix For Warner Bros

…and them wild posts (including Zillow bidding wars)

Last Sunday, James van Geelen at Citrini Research (an independent macro research publication) dropped an absolute doozy of an article.

Titled “THE 2028 GLOBAL INTELLIGENCE CRISIS” — legit in ALL CAPS — the 7,200 word piece presents a fictitious article written in June of 2028. It details how rapid improvements in AI models led to chaos in the economy. Unemployment hits Great Recession levels of over 10%. The S&P 500 sells off ~40% from current all-time highs. Private market credit tanks. White-collar workers are unable to pay their mortgages and bank balance sheets crack. Trung is still making stupid memes while his portfolio gets brutally mogged.

In a preamble, James writes “This isn’t bear porn or AI doomer fan-fiction. The sole intent of this piece is modelling a scenario that’s been relatively under-explored.”

Whether or not the Citrini article is intended as “bear porn” — aka erotica for people that want to see the market implode and profit on short positions — anytime anyone prefaces something with “this isn’t supposed to be [XYZ]”, people will inevitably perceive it as [XYX]…and that is exactly what happened.

A bunch of stocks singled out in the article puked on Monday, leading to this exchange on X:

Nathan Witkin: This is insane. Market should not be reacting like this to an economically implausible sci-fi story. That it is implies deep uncertainty and confusion surrounding AI.

Nate Silver: This is fair but deep uncertainty and confusion is probably the correct response tbh. Which is not to say there aren’t firms out there with a clearer (though not necessarily correct) thesis about AI. But the median market participant doesn’t and is going to be very vibes-based.

While some of Citrini’s assumptions may be off and the conclusions a bit fantastical, no one knows what is happening right now and a well-written narrative can capture our imaginations.

Citrini certainly delivered such a narrative and there have been ~50m views thus far.

For the purpose of this write-up, I’ll flag 6 notable themes (and add related rebuttals).

The human intelligence displacement spiral

AI agents negotiate everything…driving professional services margins to near zero

AI agents don’t give AF about credit cards

India’s consulting shops are in trouble

The $13T residential mortgage market cracks because of white-collar unemployment

The government won’t be able to respond in time

Let’s discuss.

***

1. The human intelligence displacement spiral

A few weeks ago, Anthropic and OpenAI souped up their AI coding agents with two new models: Claude Code powered by Opus 4.6 and Codex 5.3, respectively.

These have been step-change improvements in AI coding.

Citrini extrapolates the progress to mid-2026. By then, AI coding agents have become so useful that every firm re-evaluates their SaaS contracts and decides if they can build altnernative internal tools. While the in-house software doesn’t replace 100% of the features, it’s good enough that there is now leverage for every SaaS contract renewal.

In response, SaaS firms have to drop prices by 15%+. This is where it gets hairy. If SaaS firms see their margins drop, they have to fire people. Once they fire people, they replace the workers with AI agents…thus funding makers of their own demise.

That is the “displacement spiral”:

What else were they supposed to do? Sit still and die slower? The companies most threatened by AI became AI’s most aggressive adopters.

This sounds obvious in hindsight, but it really wasn’t at the time (at least to me). The historical disruption model said incumbents resist new technology, they lose share to nimble entrants and die slowly. That’s what happened to Kodak, to Blockbuster, to BlackBerry. What happened in 2026 was different; the incumbents didn’t resist because they couldn’t afford to.

With stocks down 40-60% and boards demanding answers, the AI-threatened companies did the only thing they could. Cut headcount, redeploy the savings into AI tools, use those tools to maintain output with lower costs.

Citrini called out ServiceNow in this section and the stock fell 3% on Monday.

Some Rebuttals: I recently wrote on this topic in “How does Docusign have 7,000 employees?” The code itself is only part of the B2B SaaS value prop. There’s also th built-in workflows, proprietary data, network effects, compliance, customer support and opportunity costs (most firms want to focus on their core competency and are willing to pay for useful 3rd-part software solutions).

While AI coding agents will change SaaS margins, business models and revenue flows…it will take a lot longer than 1-2 years for that to play out. Inertia is a b*tch.

Also, Gavin Baker points out, there will be a compute shortage for the foreseeable future: “The world is fundamentally short both watts and wafers and it may take years to resolve these shortages…My best guess is that we would need roughly 1000x more compute for the unlikely hypothetical scenario described by Citrini to be remotely possible and the time it takes us to get there will give humans time to adjust and maximize the many potential benefits of AI."

***

2. AI agents negotiate everything…driving professional services margins to near zero

After AI agents take on software, it moves on to other white-collar tasks. By early 2027, normies have gone all in on AI agents. They start using AI agents without even thinking of them as AI agents. The same way that people binge watch Korean cooking shows on Netflix without thinking about how they are using the “cloud”.

“By March 2027, the median individual in the United States was consuming 400,000 tokens per day — 10x since the end of 2026,” Citrini writes from the future.

One major use of these tokens: AI agents negotiating 24/7/365 on behalf of its owner.

Have you ever tried to cancel a subscription with The Wall Street Journal or The Financial Times?

It’s like pulling teeth. They grind you down to the bone. I once waited 55 minutes to cancel my FT subscription and the customer support rep convinced me to renew. I got totally pwnd. I apologized for asking to unsubscribe. Demoralizing.

AI agents won’t get demoralized and that changes everything, per Citrini:

Over the past fifty years, the U.S. economy built a giant rent-extraction layer on top of human limitations: things take time, patience runs out, brand familiarity substitutes for diligence, and most people are willing to accept a bad price to avoid more clicks. Trillions of dollars of enterprise value depended on those constraints persisting.

It started out simple enough. Agents removed friction.

Subscriptions and memberships that passively renewed despite months of disuse. Introductory pricing that sneakily doubled after the trial period. Each one was rebranded as a hostage situation that agents could negotiate. The average customer lifetime value, the metric the entire subscription economy was built on, distinctly declined.

Consumer agents began to change how nearly all consumer transactions worked.

Humans don’t really have the time to price-match across five competing platforms before buying a box of protein bars. Machines do.

These relentless agents — similar to how Kyle Reese described the Terminator to Sarah Connor (“It can’t be bargained with, it can’t be reasoned with. It doesn’t feel pity! Or remorse or fear and it absolutely will not stop!... ever... until you are dead!”) — will collapse margins for travel bookings, insurance renewals, finance advice, tax prep, routine legal work and countless white-collar professions.

Citrini thinks real estate brokers are cooked:

Even places we thought insulated by the value of human relationships proved fragile. Real estate, where buyers had tolerated 5-6% commissions for decades because of information asymmetry between agent and consumer, crumbled once AI agents equipped with MLS access and decades of transaction data could replicate the knowledge base instantly. A sell-side piece from March 2027 titled it “agent on agent violence”. The median buy-side commission in major metros had compressed from 2.5-3% to under 1%, and a growing share of transactions were closing with no human agent on the buy side at all.

Any category where the value prop is “I will navigate complexity that you find tedious” gets disrupted because the Terminator agents don’t find anything tedious.

Then, Citrini comes off the top rope with a direct hit on DoorDash:

Machines optimizing for price and fit do not care about your favorite app or the websites you’ve been habitually opening for the last four years, nor feel the pull of a well-designed checkout experience. They don’t get tired and accept the easiest option or default to “I always just order from here”.

That destroyed a particular kind of moat: habitual intermediation.

Coding agents had collapsed the barrier to entry for launching a delivery app. A competent developer could deploy a functional competitor in weeks, and dozens did, enticing drivers away from DoorDash and Uber Eats by passing 90-95% of the delivery fee through to the driver. Multi-app dashboards let gig workers track incoming jobs from twenty or thirty platforms at once, eliminating the lock-in that the incumbents depended on. The market fragmented overnight and margins compressed to nearly nothing.

Agents accelerated both sides of the destruction. They enabled the competitors and then they used them. The DoorDash moat was literally “you’re hungry, you’re lazy, this is the app on your home screen.” An agent doesn’t have a home screen. It checks DoorDash, Uber Eats, the restaurant’s own site, and twenty new vibe-coded alternatives so it can pick the lowest fee and fastest delivery every time.

I used to own the URL OnlyPhans.com. Had grand plans of turning it into a Vietnamese-focused food delivery service linking users to the best Viet eats and sultry photos of steaming bowls of broth. As much as it hurts my ego, there is literally no chance my vibe-coded OnlyPhans App is getting any traction, no matter how cheap the offering.

Meanwhile, DoorDash fell 6% on the Monday after the article dropped, even though it just recently reported its best quarter yet.

Two Rebuttals:

Byrne Hobart on why DoorDash’s moat isn’t the software…it’s the multi-sided network (Link):

DoorDash is an app for ordering food, but that's worthless without the underlying network. That network used to be loose — DoorDash famously signed up restaurants without their permission, and sold their food at a discount, but now its competitive advantages are things like having a dense delivery network (including exclusive delivery deals), accumulated data on customers and riders, and the customer support infrastructure to keep all of that running at a level of quality (an implicit SLA) that consumers have come to expect.

If you order food from DoorDash, you can be very confident that in roughly the time it was promised to arrive it'll either get there in decent condition, or you'll get a credit if the order was messed up. In a world where agents are picking the best driver and restaurant, probably by interacting with other agents, who pays whom when your meal arrives and half of the appetizer mysteriously disappeared along the way? Who sees the driver rating? Does the restaurant get a bad review, or the agent? And if the agent gets a bad review, who cares!?Ben Thompson on the stickiness of real estate broker commissions (Link):

[Citrini’s] real estate example makes the exact opposite point that the author thinks it does. The truth is that the Internet already completely obsoleted real estate agents in terms of information flow: you can go online right now and get a listing of every house for sale, with pictures, its full history, etc. There is no information asymmetry, but rather information abundance; the fact that real estate agents still exist despite that shift is actually one of the more compelling arguments that humans will be remarkably resourceful in terms of giving themselves jobs to do even in arenas where they ought to be pointless!

Furthermore, to the extent there has been any sort of compression in commissions, it’s due to the courts making it illegal to tie MLS listings to commission rates; that’s a regulatory change, not an ease-of-writing-software change, which again, makes the point that there is a lot more that goes into the economy than software and compute.Turner Novak drops a bar (Link):

"everyone will vibe code their own DoorDash" is the 2026 version of "everything will be an NFT"

***

3. AI agents don’t give AF about credit cards

Citrini continues the onslaught.

Once the AI agents destroy margins for professional services, it’ll go after an even larger pool of cheddar: the $100B+ of interchange fees that credit card companies collect every year by charging merchants 2-3% per swipe.

AI agents don’t care about credit card rewards or brand loyalty. The world of agentic commerces cares about price and efficiency…and that’s a threat to credit cards:

Once agents controlled the transaction, they went looking for bigger paperclips.

There was only so much price-matching and aggregating to do. The biggest way to repeatedly save the user money (especially when agents started transacting among themselves) was to eliminate fees. In machine-to-machine commerce, the 2-3% card interchange rate became an obvious target.

Agents went looking for faster and cheaper options than cards. Most settled on using stablecoins via Solana or Ethereum L2s, where settlement was near-instant and the transaction cost was measured in fractions of a penny. […]

Agentic commerce routing around interchange posed a far greater risk to card-focused banks and mono-line issuers, who collected the majority of that 2-3% fee and had built entire business segments around rewards programs funded by the merchant subsidy.

This was the most insane sector-specific market reaction on Monday.

Something like ~$80B in major credit card stock market cap was wiped: Visa (-4.6%), Mastercard (-5.7%), American Express (-7.2%) and Capital One (-8.8%) all got bent over.

Payments and finance folks were viscerally offended about this section of Citrini’s piece.

To be sure, credit card firms have it very cushy with interchange fees. But a lot of that money is spent on loyalty rewards, security, chargebacks and regulatory/compliance overhead.

I have friends who spend double-digit hours a week curating their credit card points like they are playing GTA 5. Even at gunpoint, they wouldn’t give up those curated Google Sheet tabs monitoring the point-levels on 38 different credit cards. They def ain’t giving that dopamine fun up to the AI agents.

A running theme in Citrini’s piece is that the text hand-waves away the hardest challenges in building a sustainable B2B SaaS business, online marketplace or payments network.

Two Rebuttals:

Kaushik Subramanian on the limits of crypto (Link):

While that article is great, I think anyone who has worked in payments can tell you that this particular excerpt is quite absolutist.

Agents need to pay [and] in order to pay, they need some form of programmable money. That could be a card in a token vault, all of which exists today. Of course they can use crypto, but the question is why? And who would take the transaction and chargeback risk in that purchase? What about 2FA?

I don’t doubt agents will buy. But I think to presume that it can only happen with crypto has a leap to be taken, and there isn’t sufficient room to take that leap.Alex Rampell on how digital payments will explode…and credit cards are still there to benefit (Link):

The payments market is going to massively expand over the next decade because:

1. ANYONE can now build anything digital — AI code creation means exponentially more digital SKUs that can be created and, of course, paid for. We are in the very early innings here. The gating item is just human creativity.

Combined with:

2. Almost anything that was “payroll” (paying PEOPLE) can now be “payments” (paying for THINGS). For example: “Hiring an assistant” or “hiring a paralegal” (both payroll) -> paying for a SKU.

We don’t think of ADP or Paychex as payments companies because they aren’t; they are payroll companies. Paying people != paying things.

But more tasks/outputs that were once only available through “paying for people” now become available for purchase on a credit or debit card. This is already starting to happen and accelerate.

***

4. India’s consulting shops are in trouble

This section may have been the consensus “most likely scenario” prediction from the piece:

[India’s] IT services sector exported over $200 billion annually, the single largest contributor to India’s current account surplus and the offset that financed its persistent goods trade deficit. The entire model was built on one value proposition: Indian developers cost a fraction of their American counterparts.

But the marginal cost of an AI coding agent had collapsed to, essentially, the cost of electricity. TCS, Infosys and Wipro saw contract cancellations accelerate through 2027. The rupee fell 18% against the dollar in four months as the services surplus that had anchored India’s external accounts evaporated. By Q1 2028, the IMF had begun “preliminary discussions” with New Delhi.

The reason this prediction rang true to many is that…IT KIND OF ALREADY IS HAPPENING.

On the Monday after the Citrini piece, Tata Consulting Services (0.45%), Infosys (-1.86%) and Wipro (-1.89%) were down but nothing wild. But these same stocks have all declined by 17%-25% so far in 2026.

The above excerpt did have one strong Rebuttal, specifically addressing the idea that the marginal cost of AI will be “the cost of electricity” (which is a crucial stat for the piece, because high marginal costs will be an obstacle to widespread AI agent usage):

Daniel Jeffries on the true marginal cost of AI agents (Link):

The marginal cost of a coding agent is not even remotely close to “the cost of electricity.”

These agents are absurdly expensive to use and run. Why do you think AI labs are banning people from having multiple $200 subscriptions? Because those subscriptions are heavily, heavily discounted to drive demand. Why did labs stop folks from using their subscription costs in OpenClaw?

The OpenClaw guy had five max subs and was losing 20k a month building and running his amazing project (because he was retired and had the money to set in fire) before AI labs banned this practice of having multiple subs.

In case you just missed it: Because these agents are expensive as hell to run.

The cost of running coding agents daily on eight hour shifts is thousands of dollars a month at API pricing and that is subsidized too…That’s not even agents running 24x7 “making money while you sleep” which is utter and total nonsense. This is one of the most spectacularly unprofitable businesses in history so far.

***

5. The $13T residential mortgage market cracks because of white-collar unemployment

Citrini pivots his predictions from the micro (company level) to the macro (wider economy).

The Human Intelligence Displacement Spiral we talked about earlier leads to wide layoffs. White-collar workers in pricey real estate markets now have to service their loans while doing gig work.

This cycle could impair $13T in residential mortgages:

Every prior mortgage crisis in US history has been driven by one of three things: speculative excess (lending to people who couldn’t afford the homes, as in 2008), interest rate shocks (rising rates making adjustable-rate mortgages unaffordable, as in the early 1980s), or localized economic shocks (a single industry collapsing in a single region, like oil in Texas in the 1980s or auto in Michigan in 2009).

None of these apply here. The borrowers in question are not subprime. They’re 780 FICO scores. They put 20% down. They have clean credit histories, stable employment records, and incomes that were verified and documented at origination. They were the borrowers that every risk model in the financial system treats as the bedrock of credit quality.

In 2008, the loans were bad on day one. In 2028, the loans were good on day one. The world just…changed after the loans were written. People borrowed against a future they can no longer afford to believe in. […]

They could still make the mortgage payment, but only by stopping all discretionary spending, draining savings, and deferring any home maintenance or improvement. They were technically current on their mortgage, but just one more shock away from distress, and the trajectory of AI capabilities suggested that shock is coming. Then we saw delinquencies begin to spike in San Francisco, Seattle, Manhattan and Austin, even as the national average stayed within historical norms.

We’re now in the most acute stage. Falling home prices are manageable when the marginal buyer is healthy. Here, the marginal buyer is dealing with the same income impairment.

A consistent criticism of Citrini’s piece is that it presents a world in which AI compresses margins for businesses…but doesn’t take the extra step to ask, “If the price of goods and services are dropping via technology-driven deflation, wouldn’t a large part of the economy benefit?”

Citrini calls the disconnect Ghost GDP:

When cracks began appearing in the consumer economy, economic pundits popularized the phrase “Ghost GDP“: output that shows up in the national accounts but never circulates through the real economy.

In every way AI was exceeding expectations, and the market was AI. The only problem…the economy was not.

In a Rebuttal, Michael Bloch shows how Citrini’s assumptions of AI progress could just as easily yield positive economic results:

Consumers spend less for more and have ample room to pay their mortgages:

Meanwhile, the purchasing power math was working in homeowners’ favor. A household whose income dropped 10% but whose non-housing expenses dropped 20% was better positioned to make mortgage payments, not worse. Debt-to-income ratios actually improved for many households despite nominal income softness, because the denominator in their monthly budget (everything besides the mortgage) had shrunk.Delinquencies ticked up in exactly the ZIP codes the bears identified — San Francisco, Seattle, Austin, Manhattan — and peaked at levels that were mildly concerning but never approached systemic. The 30-day delinquency rate for prime mortgages reached 2.1% in Q1 2028, up from 1.2% in 2025, well below the 5%+ levels that would signal structural impairment. By the time we’re writing this, it’s already declining.

Laid-off workers had easier routes to become entrepreneurs:

But the bears made an assumption that turned out to be wrong: that displaced white-collar workers would remain displaced.

What happened instead was faster and messier than anyone predicted. The same AI tools that eliminated certain roles also made it dramatically cheaper to start things. The cost of launching a business — software, legal, accounting, marketing, design — fell by 70-80% in eighteen months.

New business formation exploded. The Census Bureau reported 7.2 million new business applications in 2027, shattering the prior record of 5.5 million set in 2021. The majority were filed by recently displaced professionals who now had the skills, the tools, and the extremely low overhead to build something on their own.

Also worth flagging that B2B SaaS — despite the UX horrors it brings us everyday — makes up less than 0.5% of America’s GDP. That first industry to get clapped by AI agents won’t be enough to crater residential mortgages in 2 years.

***

6. The Government won’t be able to respond in time

Finally, Citrini writes that the speed and nature of the AI disruption will be difficult for the government’s existing policy tools to address:

Labor’s share of GDP declined from 64% in 1974 to 56% in 2024, a four-decade grind lower driven by globalization, automation, and the steady erosion of worker bargaining power. In the four years since AI began its exponential improvement, that has dropped to 46%. The sharpest decline on record.

The output is still there. But it’s no longer routing through households on the way back to firms, which means it’s no longer routing through the IRS either. The circular flow is breaking, and the government is expected to step in to fix that.

As in every downturn, outlays rise just as receipts fall. The difference this time is that the spending pressure is not cyclical. Automatic stabilizers were built for temporary job losses, not structural displacement. The system is paying benefits that assume workers will be reabsorbed. Many will not, at least not at anything like their prior wage. During COVID, the government freely embraced 15% deficits, but it was understood to be temporary. The people who need government support today were not hit by a pandemic they’ll recover from. They were replaced by a technology that continues to improve.

The widespread unemployment will fray the social fabric and turn AI labs into enemy #1.

In a Rebuttal titled “Contra Citrini7”, John Loeber thinks that Citrini underestimates the potential for the US government to re-organize the economy and deal with potential AI-induced mass unemployment:

[On] preventing a market meltdown the way Citrini imagines is actually pretty easy, and the federal government’s response during Covid showed how proactive and aggressive it is willing to be. I’d expect large-scale stimulus to kick in quickly once needed. It slightly irks me to say that it won’t be efficient, but that’s also not the point. The point is material prosperity for people in the course of their lives — broad consumer well-being that legitimizes the state and carries forth the social contract — not satisfying the accounting metrics or economic norms of the past. If we are nimble and responsive to this slow but sure technological revolution, then we will be fine. […]

My prediction is that as AI challenges white-collar labor, the political path of least resistance will be funding large-scale re-industrialization in the form of employment megaprojects which, thankfully, are not subject to a singularity but rather move at the friction-heavy speed of getting things done in the physical world. We'll build bridges again.

People will find it gratifying to see the fruits of their labor in the real world, not in digital abstractions. The Senior PM at Salesforce that loses their $180K job might find a new job in the field at the California Desalination Works, to finally, finally, end the 25-year drought. And it shouldn't be good enough, but excellent. And once it is built, it must be maintained! Once more, Jevons Paradox can apply, if you allow it to.

Meanwhile, Tyler Cowen breaks down why there won’t be a demand problem if AI is delivering super-high productivity growth (think GDP growth of 10%+ a year):

If AI produces a lot more stuff, income is generated from that and the economy keeps going, whether or not the resulting distribution pleases your sense of morality. Along the way, prices adjust as need be. If unemployment rises significantly, prices fall too, all the more. I am not saying everyone ends up happy here, but you cannot have a) a flood of goods and services, b) billions accruing to the AI owners, without also c) prices are at a level where most people can afford to buy a whole bunch of things. Otherwise, where do you think all the AI revenue is coming from? The new output has to go somewhere…

Besides, why assume that “the machines” here are reaping all the surplus? Are they the scarce factor of production? Maybe it is hard to say in advance, but do not take any particular assumptions for granted here, ask to see them spelt out. One simple scenario is that the regions with energy and data centres become much wealthier, and people need to move to those areas. Maybe they do not do this quickly enough, a’la our earlier history with the Rust Belt. That is a problem worth worrying about, but it is nothing like the recent collapse concerns that have been circulating.

On the redistribution front, Alexander Campbell has thoughts on how governments will have to change tax systems. If capital takes more share of GDP, then we may have to refocus the tax base away from labor to capital and compute (“If AI collapses labor’s share of GDP, a tax system built on taxing labor income is dead. Tax capital directly. Not punitive, just following the money.”)

If you’re really fixing for more macro-economic Rebuttals, enjoy this point-by-point takedown by Citadel Securities (aka one of the world’s largest market makers) titled… wait for it…“The 2026 Global Intelligence Crisis”. Honestly, kind of insane they felt compelled to respond. Speaks to the wild uncertainty of the current moment.

***

Final Thoughts

Go read the Citrini piece if you haven’t.

I didn’t talk about the section on how private equity will blow up because of its significant enterprise SaaS investments that go bust.

Blackstone, KKR and Apollo all got clapped on Monday after the article.

In the past two weeks, we have now had two nuclear viral AI doomer articles.

The concluding bit of Citrini’s article talks about the commoditization of intelligence (and I think it points to why these doomer narratives keep going viral:

For the entirety of modern economic history, human intelligence has been the scarce input. Capital was abundant (or at least, replicable). Natural resources were finite but substitutable. Technology improved slowly enough that humans could adapt. Intelligence, the ability to analyze, decide, create, persuade, and coordinate, was the thing that could not be replicated at scale.

Human intelligence derived its inherent premium from its scarcity. Every institution in our economy, from the labor market to the mortgage market to the tax code, was designed for a world in which that assumption held.

We are now experiencing the unwind of that premium. Machine intelligence is now a competent and rapidly improving substitute for human intelligence across a growing range of tasks. The financial system, optimized over decades for a world of scarce human minds, is repricing. That repricing is painful, disorderly, and far from complete.

This is the most important premise in the piece.

It might not be 1-2 years. But, within a decade? Seems reasonable and the availability of human intelligence on tap (or as Dario says, “a country of geniuses in a data centre”) will change every facet of society.

The only consensus as to how this unfolds…is that there is no consensus (and we are all out here making wild ass guesses).

“The fact that a piece of AI science fiction rocked the stock market this week is a clear indication that absolutely no one knows how the next few years will go,” writes Derek Thompson.

Thompson elaborates:

I do not mean that AI architects are stupid. I do not mean that their speculation is absurd or worthless. I certainly do not mean that they don’t have access to narrow truths, such as rising adoption of AI in general and autonomous “agents,” in particular.

What I mean is that the frontier labs don’t really know what they’re building exactly, and economists don’t know how to model the thing that they claim they’re building. As a result, nobody really knows what is going to happen with AI this year, or next year, or the year after. There is no secret cigar-filled room of elites who have unique access to some authentic postcard from the future.

And a compelling narrative will fill the void, especially with so many of the AI industry’s deciders congregated on X waiting to fling around hot takes (for real, 500-1000 of the most important people funding and building our AI future are addicted to the artist formerly known as Twitter and posting non-stop).

For three days, people were cooking Citrini Research for saying — if we take the least charitable take — that DoorDash and Visa were done because your grandma could vibe code a replacement.

Then, Thompson’s perspective that “no one knows” was hammered home on Thursday when Jack Dorsey announced that Block was firing 40% of the company (headcount fell from 10,000 to 6,000).

Dorsey cited AI: "The core thesis is simple. Intelligence tools have changed what it means to build and run a company. We're already seeing it internally. A significantly smaller team, using the tools we're building, can do more and do it better. And intelligence tool capabilities are compounding faster every week."

The timeline filled with competing takes on whether it was a proper rightsizing after mismanagement (recall that Dorsey ran Twitter and that company is now 80% smaller in terms of headcount post-Elon). Or if the Block cuts were truly for AI efficiency gains…Dorsey even jumped in on X to clarify the point.

Block gained +25% on the news, which means other CEOs may want to copy the playbook and cite AI whether or not it’s the real reason (aka “AI washing”).

Whatever the rationale behind the Block case, there will absolutely be more viral AI doomer stories and viral “AI is breaking the economy” stories to come.

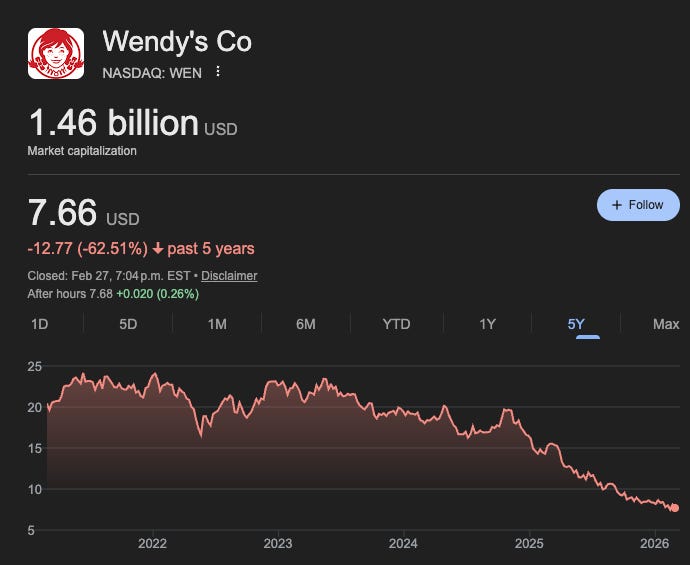

Some joker is probably writing a “State of the Market June 2029” article predicting the end of Wendy’s because AI agents only like round burger patties.

I will read it (and probably buy call options on Burger King and McDonalds).

I will read them all and try to keep a level head about it.

But just in case the AI agent doomer bear porn is true, I recently went down to the Apple Store…

This issue of SatPost is brought to you by Bearly AI

Are you looking for a no-logging, encrypted and anonymized AI chat tool?

Then try the Bearly AI research app, which provides an easy-to-use UX for the newest models from OpenAI, Anthropic, xAI, DeepSeek, Gemini and more.

While some AI providers keep chat logs indefinitely even after a user deletes them...Bearly AI has a default no-logging policy and user chats are encrypted while requests to LLM providers are completely anonymized.

Try one month FREE of the Pro Plan using the code BEARLY1.

Norway’s Sporting Secret Sauce

Norway won the most Gold (18) and total medals (40) at Milan Winter Olympics.

It’s the 4th straight Olympics that Norway has topped the list…in a country of only 5.6 million people.

Yes, a lot of those medals were in cross-country skiing.

But there’s clearly something going on up there.

Author Brad Stulberg has a great explainer, and a major part is how Norway approaches Youth Sports (very different than in North America):

1. Scorekeeping:

In the US: Youth sports tend to be hyper competitive even at early ages. Leagues almost always keep score.

In Norway: Scorekeeping isn’t even allowed until age 13.

Removing winners and losers keeps the focus on the process not outcomes. It keeps kids engaged longer because it minimizes pressure (and tears) and maximizes fun, learning, and growth. The goal isn’t to win a third grade championship. It’s to love sport and keep playing.

2. Trophies:

In the US: If you give everyone a trophy, you’re creating snowflakes who will never gain a competitive edge.

In Norway: Whenever trophies are awarded, they are handed out to everyone.

If getting a trophy makes young kids feel good, we should give them trophies. Maybe they’ll come back and play again next year!!

As for the creation of snowflakes with no competitive edge — Norway’s athletes are tough as nails and all they do is win.

3. Prioritizing Fun:

In the US: Far too often, the goal is to win.

In Norway: The national philosophy is “joy of sport.”

Youth sports in the US are driven by adults, ego, and money. Youth sports in Norway are driven by fun.

Only half of kids in the US participate in sports. The number one reason they drop out: because they aren’t having fun anymore. In Norway, 93% of kids participate in youth sports. Fun is the foremost goal.

4. Playing Multiple Sports:

In the US: There’s pressure to specialize early and play your best sport year round.

In Norway: Try as many sports as you can before specializing as late as college.

Norway encourages kids to try all types of sport. This reduces injury and burnout and increases all-around athleticism. It also helps promotes match quality, or finding the sport you are best suited for as your body develops, which is impossible if you commit to a single sport too early.

5. Affordability

In the US: There is increasingly a pay-to-play model with high fees for leagues, equipment, and travel. This excludes many kids from playing.

In Norway: It’s a national priority to keep youth sports affordable and therefore accessible for all.

Kids aren’t priced out, which creates opportunities for everyone to participate (and develop into athletes), regardless of their parents’ income level.

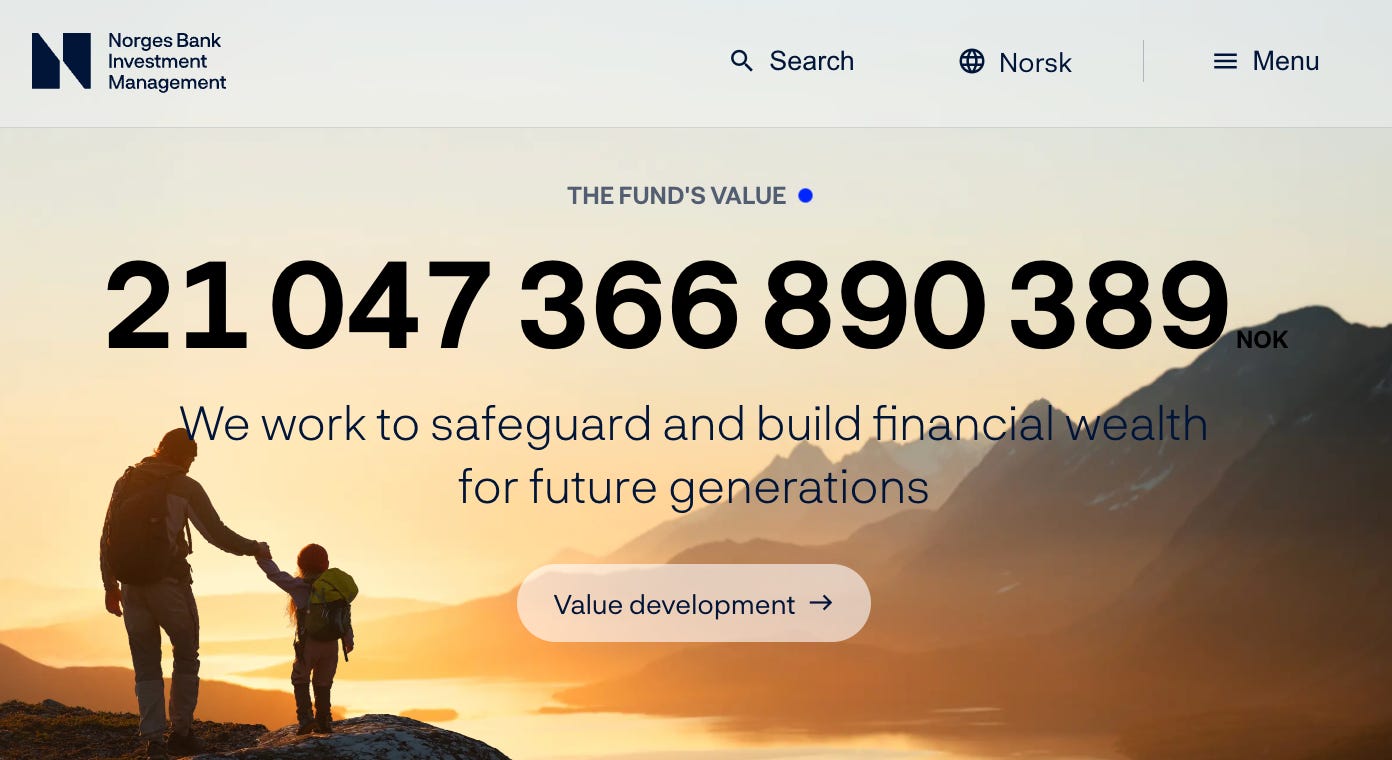

For Norway, the Olympics sporting success maintains a streak of impressive counting stats, including a dynamic UX landing page for its sovereign wealth fund (which keeps real-time tracker of value).

It’s now ~$2T and owns 1.5% of global equities (worth $357k per citizen and up more than 6,000x since the fund received $300m in 1996…from off-shore oil revenue first found in 1969).

About 3% of the fund is spent every year for the country’s infrastructure and that no doubt helps the sporting results. But Norway’s Olympic outcomes outperform even on a per capita dollar spent basis.

Anyway, Nicolai Tangen — the CEO of Norwegian Sovereign Wealth Fund — was recently on The Knowledge Project podcast and dropped some management alpha.

Tangen keeps an ice cream stand by his office so people randomly come and he just catches up with them. Says ROI on the ice cream is in the 1000x.

Another high ROI move is being the CEO of a $2T fund…because that might be the best hack ever for getting people on your podcast (Tangen’s In Good Company podcast is very good…check this one with Stanley Druckenmiller).

Paramount Outbids Netflix For Warner Bros

What a roller coaster!

Paramount and the Ellisons have officially outbid Netflix to buy Warner Bros. studio and cable assets. The deal values Warner Bros at $82B and Paramount will also take on the company’s ~$30B in debt.

To close the deal, the combined Paramount and Warner Bros will see a net debt of $70B…which is why they are already talking about $6B in cost savings “synergies” and — after briefly freaking out about Netflix’s commitment to the theatre system — Hollywood actors, agents, writes and directors are now freaking out about Paramount cuts (Ellison has committed to release a juicy 30 films a year).

The new Ellison empire is formidable. It has CNN and CBS News. Dozens of TV networks. All of March Madness. The UFC. And IP galore:

Paramount: Star Trek, Mission: Impossible, Transformers, SpongeBob SquarePants, South Park, PAW Patrol, Top Gun, and the “Sheridan-verse” (Yellowstone, which they keep even after the director moves to Universal).

Warner Bros: DC Universe (Batman, Superman, Wonder Woman), Harry Potter, Lord of the Rings, The Matrix and the legendary HBO (Sopranos, The Wire, Succession, Silicon Valley etc)

Please please please give us a mash-up between South Park, The Sopranos and Paw Patrol.

As discussed on the The Town podcast, this deal will have to still go through anti-trust review but the Ellisons closeness to the current White House suggests they’ll pull it off. European and state regulators can still gum it up, though.

With a combined 219m subscribers (some are def double counted), Paramount+ and Max can legit give Disney+, Netflix and Prime a run for their money.

The undoubted winner of all: Warner Bros Discovery CEO David Zaslav. He walks with a $500m+ golden parachute payout AND got Paramount to pay Netflix a $2.8B deal termination fee out of its coffers (BTW, $2.8B was straight profit and equal to 25% of Netflix’s entire profit of $11B in 2025).

That’s a solid consolation prize for co-CEOs Ted Sarandos and Greg Peters…and they could do the funniest thing ever with those funds.

Back to Zaslav, he originally ran the Discovery cable network between 2006 and 2022, overseeing a GOAT-level run on personality-driven reality TV delirium: Deadliest Catch, Mythbusters, 90-Day Fiancee, Jon & Kate Plus 8, Property Brothers and Fixer Upper etc.

When A&T failed its Warner Bros project, Zaslav was waiting to graduate to films and make real hay in Los Angeles.

I imagined Zaslav was thinking, “I gotta level up from this TV slop and go full Hollywood, including buying the 8-figure mansion formerly owned by Hollywood legend and Paramount producer Robert Evans…who was instrumental in getting The Godfather made.”

Well, he did all of that.

Because, in 2022, Zaslav spearheaded the merger of Discovery with WarnerMedia and became the CEO of Warner Bros. Discovery. The plan was to take Discovery’s assets and combine with with Warner’s legendary IP into a Netflix competitor.

The strategy looked bust by early 2025.

Weighed down by debt and the dying TV cable bundle, the value of Warner Bros. Discovery sank by more than half from its IPO to ~$20B.

Enter David Ellison.

Along with his father Larry’s $200B backstop, David had a mission to build a next-generation media, streaming and technology juggernaught (Oracle + a TikTok stake + Paramount + AI stuff).

Last summer, he closed a deal for Paramount and immediately set his sights on Warner Bros. By combining Paramount+ with Max, he could create a scale streaming service to take on Netflix.

As we all know, Netflix wasn’t going to let that happen lying down.

What ensued was a bidding war that saw ~10 bids over 4 months. Most of it was Paramount just pumping the price.

Netflix’s best offer was $72B equity for just the Warner Bros film and TV studio. The cable TV assets were to be spun off this fall. Paramount long held it had the better deal because Netflix was overvaluing the value to shareholders of those cable assets.

Ultimately, the potential spin off was moot. Paramount eventually pushed its offer valuing Warner Bros at $50B (including debt) to $82B of equity (and $110B enterprise value overall).

The 66-year old Zaslav was able to juice the value of Warner Bros, all while Netflix and Paramount both saw sell-offs of 30%+ (shareholders terrified by the debt).

Dude legit pulled a rabbit out the hat.

Paramount & Warner Bros is a major player but they still have a tough hill to climb…

Links and Memes

Anthropic vs. Department of War: As I write this, there is an ongoing dispute between Anthropic and Secretary of War Pete Hegseth. Anthropic has specific terms of services that disallow: 1) mass surveillance; and 2) use of its technology for fully autonomous machines that can kill (without a human in the loop).

The tension is over whether a private company can limit the scope of government national security requirements. Secretary Hegseth wants those terms removed and is threatening some very powerful policy tools to get the outcome.

This is a very very important issue with the power of AI and its use on the battlefield.

On Friday afternoon, Secretary Hegseth labelled Anthropic a supply-chain risk — a tool meant for foreign adversaries — and President Trump issued an order giving government agencies 6 months to move to other providers (OpenAI and xAI have agreed to Department of War’s conditions).

“Effective immediately, no contractor, supplier, or partner that does business with the United States military may conduct any commercial activity with Anthropic,” Hegseth wrote on X. “Anthropic will continue to provide the Department of War its services for a period of no more than six months to allow for a seamless transition to a better and more patriotic service.”

Dario Amodei may still continue discussions in coming days. But, right now, Anthropic is on the way out and the implications are massive. The government is only responsible for $200m of Anthropic’s total $15B+ revenue. But any contractor working with the government may have to choose between that public contract and the AI lab.

One major example: Amazon — which owns 15-20% of Anthropic (and serves its models) — and has a multi-billion government contract with AWS. Google and Microsoft also serve Anthropic…while also being government contractors. How will this shake out?

Anthropic responded by saying that the “supply chain risk” only legally applies to Department of War contracts. Meanwhile, OpenAI has struck an agreement the government to deploy across the government’s classified networks.

More updates to come but here are key links:

Zvi Moshowitz has a round-up of positions from major players involved.

Palmer Luckey explains how terms of services allow corporations with unelected leaders to potentially dictate national security objectives (and why he is against them doing so)…notably, Anthropic had previously chosen to deeply embed into the government’s classified networks and allow the model use for defense up to everything (except for the red lines it has since drawn).

Dean Ball believes this sets a very bad precendent and an overreach by the government (if the government doesn’t want to work with Anthropic, it can choose not to do so…but doesn’t have to hit the company severe penalties: “The way to enforce this principle is to publicly and proudly decline to do business with firms that don’t agree to those terms. Cancel Anthropic’s contract, and make it publicly clear why you did so.”)

Just Another Pod Guy makes the point that no matter how one feels about the terms of service, the government can escalate to restricting GPUs if deemed national security…which is the ultimate ace in negotiations with the AI labs.

Beff Jezos discusses how the effective altruists were pushed out of OpenAI (and still primarily operate in Anthropic)…and how that’s all potentially playing into all of this.

***

Some other links for your weekend read:

Some made a game called “Data Centre” on Steam…imagine first-person shooter games with cables and server racks instead of guns. We are reaching new levels of AI hype.

A guy accidentally got control of 7,000 DJI robot vacuums…because he wanted to hack the one he bought to run on a PS5 controller LOL.

Floyd vs. Manny 2…Netflix got the two legendary boxers to fight for a 2nd time at the Sphere in September. The news reminded me of that time Manny bumped into Floyd at a Lakers game a few year after their 2015 fight (they split $400m) and just looked at each like “bro, we made so much money”

Investing legend Stanley Druckenmiller…did a 30-minute with Morgan Stanley and talked about his “invest then investigate” approach as it relates to Nvidia. He made a bet without even knowing “its earnings” because smart people in his network mentioned it. Then, as he learned more, kept doubling. Made a 6x in a few years but said he exited too soon. He self-deprecatingly says he IQ isn’t top top, but his superpower is knowing when to “pull the trigger”. Great chat.

Prediction platform Kalshi banned and fined…one of MrBeast’s producers for trading on insider information related to a prediction market about the mega-YouTuber.

Burger King is launching this AI chatbot called “Patty”…that talks to employees through the headset. The AI clarifies what to cook and reminds the employee to say “Welcome to Burger King”, “please” and “thank you” to customers during interaction points. What are we doing here?

…and them wild posts:

Skillfully summed up. Key takeaway is that no one really knows where are headed. Fascinating times. Time to go open a restaurant or a gas station XD

That was a nice summary! You must spend a sick amount of time on these writeups! Also found the summary of what DocuSign does fascinating. Since they have gone from 7,000,000 to 7000 employees, I think it's now a buy!!