Live Nation x Ticketmaster Monopoly, explained

PLUS: Bieber Takes Over Coachella, Jensen vs. Dwarkesh and Allbirds AI pivot.

Thanks for subscribing to SatPost.

Today, we will talk about Live Nation: a federal jury determined the $36B live events giant operates an illegal monopoly and may force the company to spin off Ticketmaster.

Also this week:

Bieber Takes Over Coachella

Should Jensen sell Nvidia chips to China?

…and them wild posts (including Allbirds)

A few weeks ago, we talked about Disney and how the company’s reliance on its theme parks & cruises division is warping the entire business. The division has grown from 18% to 57% of Disney’s operating profits over the past decade (while still only 1/3rd of total revenue).

Disney has to milk park attendees with egregious prices, because it needs the cash to navigate the transition from cable TV to streaming (hence, the 100x marked-up Mickey Mouse ears and the $250 lightsaber that I was very very close to buying).

Now, let’s talk about Live Nation and its subsidiary Ticketmaster. This week, a US federal jury found that Live Nation illegally maintained monopoly power in the market for large amphitheatres while Ticketmaster did the same for ticketing at major concert venues.

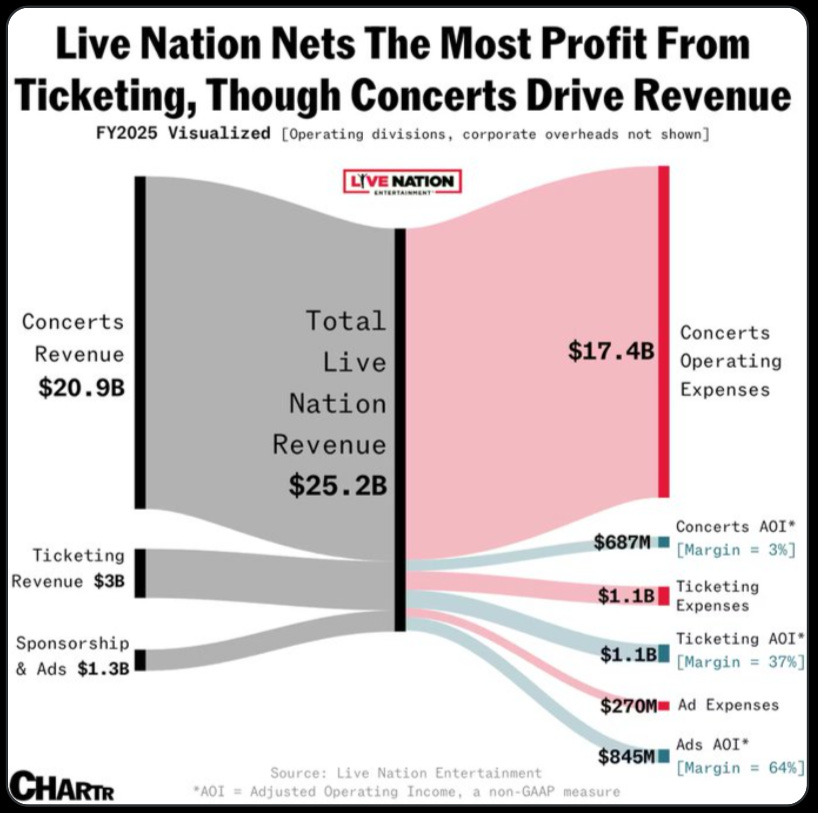

To understand how these monopolies work, let’s start with this visualization of Live Nation’s revenue and operating profit via Sherwood News.

For more context, Live Nation is the world’s largest promoter and producer of live events (booking, marketing, logistics etc). It owns or has a stake in ~400 major concert venues across the world.

Since acquiring Ticketmaster in 2010, Live Nation’s stock is up 17x to a market cap of $36B (naturally, I missed out on every single part of this run-up).

In 2025, the company put on 55,000 events. It manages 400 artists including Madonna, Lady Gaga, Miley Cyrus, Post Malone and Weezy F Baby (owning 65% of the concert promotion market) and sold 646 million tickets (Ticketmaster controls 86% of the ticketing market for major venues and sold 10x more tickets than the 2nd place AEG).

Of those ticket sales, 53% (or 346 million) included fees.

Live Nation’s revenue hit a record $25.2B last year (compared to $7.3B in 2015) and its three main income streams are concerts, ticketing and sponsorship & ads.

Across these divisions, the difference between revenue and profit is even more extreme than Disney.

In 2025, the concert division did 83% of Live Nation’s revenue ($20.9B) but — with a tiny margin of 3% — it only contributed 26% ($687m) to the company's $2.6B in adjusted operating profit.

Live Nation’s other two divisions operate with much higher margins:

Ticketing (37% margin): 12% of sales ($3B of $25.2B) and 42% of adjusted operating profits ($1.1B or $2.6B).

Sponsorship & ads (64% margin): 5% of sales ($1.3B of $25.2B) and 32% of adjusted operating profits ($845m of $2.6B);

If Disney is squeezing parks & cruises to the detriment of park attendees — granted, without any antitrust heat — which Live Nation division do you think is squeezing customers?

Is concerts? Is it ticketing? Or sponsorships & ads?

We all know.

But if you’re still on the fence, here is one of the most on-point tweets in the history of Twitter:

Ok, it is a bit more complicated than “Might as well fee”.

But Ticketmaster’s fee situation is definitely the most salient and consumer-facing part of the key antitrust charges…and ticketing has been key pillar for past decade:

Here is more from Music Business Worldwide:

Across three core claims [against Live Nation], the jury found that:

Ticketmaster willfully acquired or maintained monopoly power in the market for primary ticketing services to major concert venues through exclusionary conduct.

Ticketmaster did the same in the market for primary concert ticketing services to major concert venues.

Live Nation willfully acquired or maintained monopoly power in the market for large amphitheaters through exclusionary conduct.

In each case, the jury also found that the anticompetitive conduct caused harm, and that Live Nation controlled, dictated or encouraged Ticketmaster’s behavior.

The jury additionally found that Live Nation unlawfully tied artist promotion services to the use of its large amphitheaters (meaning artists were required to use Live Nation’s promotion services in order to play its amphitheaters).

On damages, the jury found that consumers were overcharged by $1.72 per ticket for primary concert tickets at major concert venues across 22 states and the District of Columbia [this $1.72 overcharge applied to ~20% of all Live Nation tickets sold].

According to the states’ case, Live Nation is using its monopoly position to basically Tony Soprano everyone in the ecosystem:

To the artists: “Oh, nice tour you have there, would be a shame if we didn’t promote it because you used a 3rd-party venue.”

To 3rd-party venues: “Oh, nice stadium you have there, would be a shame if it stays empty because we won’t let our artists play there unless you use our ticketing platform.”

To fans: “Oh, nice college fund you have there for your kid, enjoy this Another Dollar Won’t Hurt Fee because what other ticketing platform will you use to book your favourite artist who we happen to rep?”

To be sure, these concerns have existed for decades.

As Matt Stoller highlights, Ticketmaster’s webpage basically brags about absorbing a competing platform in 1991 right on the timeline page of its website: “Ticketmaster acquires its major competitor Ticketron”.

They were rolling up other ticketing platforms to gain market power.

In 1994, Pearl Jam went to war against Ticketmaster. Stone Gossard and Jeff Ament — along with the managers for Aerosmith and REM — testified in congress against the ticketing giant. The artists said that Ticketmaster was using its influence over venues, promotion and tickets to charge fans “exorbitant fees”.

Pearl Jam ended up cancelling its tour that year due to this beef.

While Ticketmaster was cleared of being a monopolist in various class-action lawsuits, its reputation hasn’t exactly…well, please see the above tweet.

When Live Nation acquired Ticketmaster in 2010, the Department of Justice (DOJ) forced the newly formed company to pinky swear sign a 10-year consent decree agreeing not to force concert venues to use Ticketmaster. In 2019, that consent decree was given more meat because venues were complaining that Live Nation was retaliating against them for using other ticketing platforms.

Then, came the “website crash heard around the world”. On November 15, 2022, a super-duper-superstar artist who rhymes with Baylor Sift launched the Eras tour. A record 2.4 million people bought tickets on Ticketmaster that day but millions of other fans were left in the lurch and the website went down.

A bunch of Swifties then got rugged on secondary markets by scalpers and the outcry led to lawsuits and another congressional hearing. Within two years, the DOJ and dozens of states had filed antitrust lawsuits against Live Nation.

Live Nation settled its lawsuit with the DOJ just last month. However, the states case kept going and that is how we got this week’s legal outcome.

That earlier settlement provides a roadmap for how a judge may seek antitrust remedies against Live Nation.

But, first, I want to play some devil’s advocate.

I’m personally biased against all ticketing platforms (Ticketmaster, StubHub, SeatGeek) for two reasons. First, we’re obviously getting donged on the fees. Second, anytime I have to buy a ticket on the secondary market, it is a reminder that I don’t have the hustle to actually snag a ticket right when it goes on sale (I’m learning this lesson the VERY VERY hard way with FIFA 2026 tickets right now).

So, I had to force myself to understand Live Nation and Ticketmaster’s rationale for their tie-up (a "steelman" if you will):

Organizing and promoting live concert events is very expensive and has paper-thin margins. Dude, I can barely organize a coffee meeting. I can’t imagine the lift that goes into throwing a concert for The Weeknd. A fully-integrated business — with control of ticketing that ties promotion and ticket inventory — creates a better fan experience and is the most viable way to make the whole model work for everyone long term.

A scaled player can invest more in infrastructure, fraud prevention, resale controls and digital ticketing (I will admit that the Ticketmaster App is pretty slick and it feels like magic when a concert ticket shows up in Apple Wallet).

Live Nation doesn’t actually set most of the ticket price. Artists dictate the face value and venues tack on most of the Fee-Fees (80% of Live Nation events are in 3rd-party venues).

The last point probably has the most credence.

Yes, ticket prices have definitely gone up. According to Bloomberg, the average face value price for a top-100 artist has risen from $53 in 1996 to $142 today (all adjusted for inflation).

There are a few key factors to consider about this price increase.

In the 1990s, concerts were marketing for the physical albums. CD sales — aka the bundling of 2 or 3 great songs with a bunch of filler no one wants — was an incredible business model for artists. Physical albums were the cash cow.

Now, live touring makes up the majority of income (70%+) for the top-tier artists and streaming services are the marketing tool to get people to come to the shows. Artists are very incentivized to pump them ticket prices and the demand for live events has been wild post-COVID.

Those pesky secondary markets also (shocker) inflate ticket prices….especially from fees. For primary tickets, fees are ~27% of the face value. On secondary markets, one study found fees hitting 56% of a ticket’s face value.

The clear appetite of buyers on the secondary market has led to platforms implementing dynamic pricing, which further boosts primary ticket prices (but at least this money is going to artists and promoters, opposed to scalpers).

This is a long way of saying that Live Nation isn’t the only one milking fans. The company is a pain sponge for the rest of the industry (similar to how Roger Goodell gets paid $70m a year to eat shit for the NFL owners).

But but but but, let’s be honest. They is milking us with them fees. Of course they are. Look at the business model. Just like Disney with Disneyland. Live Nation has to turn the fee dial if it wants to profit-maxxxx.

There were some pretty damning evidence from the state’s antitrust trial, per NYT:

Live Nation employees joked about trying to “gouge” people for parking and V.I.P. upgrades at concerts, calling fans “so stupid” for paying the inflated charges and boasting that they were “robbing them blind baby.”

To quote one of the greatest fictional characters in the history of the TV medium: “Is you taking notes on a criminal f-cking conspiracy?"

The company’s explainer via Bloomberg:

Live Nation’s ticketing director Ben Baker testified that Ticketmaster’s fees depend on the face value of the ticket. As of September 2023, the company’s standard rate card called for charging $3.25 on tickets with a face value of as much as $5.99. From there, the fees increase based on face value with the highest price range — above $116 — garnering a 20% fee that caps at $70.

Will Live Nation be broken up?

The stock was up +3% in the day after the verdict. Markets don’t seem to think the judge will force Live Nation to divest Ticketmaster. It would be gnarly. Recall, the concert division made $687m on a $20.9B revenue for a paltry margin of 3%.

WHAT IS THIS? AN OPERATING MARGIN FOR ANTS?

The current vibe feels similar to Google losing antitrust cases in the past two years, with courts deeming that it illegally operates search and ad network monopolies. However, Google avoided a break-up (which would have included a spin-off of Chrome). The search giant was forced to make changes to distribution deals and data sharing but most considered it a “slap on the wrist”. The judge said he didn’t want to disrupt a rapidly changing market (aka AI and the rise of OpenAI/Anthropic is threatening Google).

Breaking up Live Nation wouldn’t be nearly as disruptive, though. And the company has clearly abused its position…so who knows?

Live Nations has already signalled that it will appeal the decision.

Either way, the settlement with the DOJ last month is probably the template: it paid a $280m fine, will divest from 13 venues, offered ticketing platform interoperability and agreed to a 15% cap on service fees at Live Nation-owned venues.

If there isn’t a break up, we’ll probably see more divestitures and get a lower cap on service fees (and an application of that cap across every venue on the Ticketmaster platform, not just Live Nation-owned ones).

The ticketing division would remain Live Nation’s profit engine...but with fewer Cuz We Can Fees.

This issue of SatPost is brought to you by Bearly AI

Are you looking for a no-logging, encrypted and anonymized AI chat tool?

Then try the Bearly AI research app, which provides an easy-to-use UX for the newest models from OpenAI, Anthropic, xAI, DeepSeek, Gemini and more.

While some AI providers keep chat logs indefinitely even after a user deletes them...Bearly AI has a default no-logging policy and user chats are encrypted while requests to LLM providers are completely anonymized.

Try one month FREE of the Pro Plan using the code BEARLY1.

Bieber Takes Over Coachella

Speaking of live music events, the Super Bowl for Molly Coachella music festival hosts is wrapping up its second weekend. The event is actually put on by Live Nation’s main competitor AEG.

The buzz from last weekend was headliner Justin Bieber doing a stripped down set on Saturday. People thought it was lazy and unbecoming of his $10m payday across two performances. Particularly, after Sabrina Carpenter put on a Broadway-caliber set on Friday.

Disclaimer: My wife calls me Top 40 Phan and I am a huge Bie-lieber. Been a fan for nearly two decades. Gun to my head, his best tracks are “Despacito (Remix)”, “Beauty and the Beat”, “What Do You Mean”, “Never Say Never”, “Somebody To Love (ft. Usher)”, and “Baby".

“Mistletoe” is also my favourites Christmas song ever (like I said, I’m an OG supporter…and Top 40 Phan).

I wanted to stay up for the YouTube livestream but, hahahhaha, c’mon man. It started at 11:35pm. My kid has sports on Sunday morning.

Anyway, I woke up Sunday and Bieber had taken over the entire timeline. People were absolutely cooking him for spending a portion of the performance sitting at a table with a laptop while scrolling through memes and a bunch of his old YouTube music videos.

I added my $0.02 that no one asked for.

After bathing in some dopamine from this post, I watched the set and was very very wrong.

The YouTube stuff was perfect: So much of Bieber’s career is tied to the platform. In 2008, Scooter Braun famously discovered Bieber in a YouTube video singing to Chris Brown’s “With You”. In 2014, “Baby” became the second YouTube video — after “Gangnam Style” — to cross 1B views. At Coachella, he watched both songs and duets with the videos among others.

Oh, and YouTube is Coachella’s official global livestream partner. Shocker, Bieber rehearsed the entire moment, which many people thought was super authentic and organic.

In reality, Bieber was a massive get for Coachella.

The largest music festivals (Coachella, Glastonbury, Lollapalooza) and the broader industry have been in a weird spot. It’s estimated that 90 such festivals were called off in 2024 and another 50 in 2025. A lot of these event organizers probably overestimated the post-COVID comeback of “live events”.

For the world’s biggest artists (Taylor Swift, Rihanna, Beyonce, Coldplay), Coachella doesn’t actually make a ton of sense anymore. These acts can pull $10m+ per night on their own tours.

Trapital’s Dan Runcie wrote about the Coachella business in 2023 and explained how the festival pays artists:

Headlining the show is great for many superstar artists, but at the highest heights there’s a tradeoff. In recent years, the headliners get $4 million per weekend (but I heard from a source that Bad Bunny got $5 million). The artist on the second row got $750,000 per weekend. That’s a great payday, even for an artist selling out arenas. But for an artist like Taylor Swift, who can likely gross $10 million per night on her own stadium tour, then she may be leaving money on the table. This is where the Coachella documentary deals play a factor. Beyonce was rumored to be paid $20 million for the Homecoming documentary on her 2018 show, which made the experience worthwhile for her (and the Beyhive).

For other artists, Coachella is a brand-building signal to keep getting looks. Cardi B performed in 2018 and was paid just $70,000 per weekend. She spent more on her production, but she saw it as an investment. Cardi now gets paid $1 million for private shows regularly. She used a Coachella performance the same way a speaker uses a TEDx Talk. Sure, they weren’t paid. But that high-quality video lives on YouTube forever and will be the proof point to land more lucrative speaking and career opportunities.

Bieber has had a rocky few years but the comeback vibe has been strong in 2026.

He did a viral Grammys performance in February and now Coachella. If this catapults him back into top-top-tier, then it worked out for everyone.

I might stay up to watch Bieber’s second Saturday live because he could do the most glorious thing ever: just sit on the stool and play last Saturday’s entire 90-minute performance on YouTube. Do it Beibs! I belieb in you.

Links & Memes

Should Jensen sell Nvidia chips to China? Jensen Huang went on the Dwarkesh podcast and it got spicy. Dwarkesh asked very good questions and kept pressing on key topics.

At about the 1-hour mark of the podcast, Dwarkesh asks Jensen whether Nvidia should sell chips to China. The US government has had export controls in the past few years and Nvidia went from 90%+ market share of AI compute in China to less than 50%. Meanwhile, Chinese networking giant Huawei has made serious headway.

The exchange led to what many on X called the most Rorschach Test in recent memory. Split between those that agreed with Jensen and those that agreed with Dwarkesh.

Dwarkesh made the argument for why America — especially after the recent release of Anthropic’s Claude Mythos model with significant cybersecurity capabilities — should not allow China to have access to Nvidia’s best chips. He was coming from the camp that AGI/ASI may happen next few years and it’s crucial America does everything to win that race.

Jensen is a lot less “AGI-pilled” and frames the situation in much more business and market share terms. You could tell that Jensen was speaking to a number of constituents (shareholders, the public, US government, Chinese government) with his answers. Many felt he never addressed Dwarkesh’s key assertion that giving China access to top-tier chips would be a national security threat.

The point that Jensen has made for years is that if China doesn’t get access to Nvidia’s chips, an entire domestic ecosystem will develop and that ecosystem will ship to the rest of the world. As in, the majority of people will use the “Chinese Tech Stack” instead of the “American Tech Stack”. That is both a commerce and geopolitical concern.

Jensen’s argument made ALOT of sense before the export ban started. Let’s get China hooked on Nvidia chips and the American Tech Stack. But since the export ban started in October 2022, the CCP has 100% committed to creating a fully indigenous semiconductor industry whether or not the country ever imports any more Nvidia chips.

From here, my thinking was: “If China is going to to speedrun a semiconductor industry no matter what, a geopolitical rival shouldn’t help it…so, yeah, America should ban all Nvidia chip exports”.

Also, since the manufacturing of chips is a bottleneck…that meant any chips shipped to China was less for America and Western allies.

After listening to the podcast twice and reading all the commentary — it went mega viral (including a wild moment when Jensen kinda lost it and dropped this line, “I didn’t wake up a loser”) — I have changed my mind.

Nvidia should definitely NOT send the best chips to China. However, there is a point on the spectrum between “send 0% of chips” and “send 100% of chips” that Jensen is trying to hit. Obviously, it’s self-interested. He cares about Nvidia’s global market share. If Huawei builds a complete parallel AI system, that will be bad for Nvidia in the long run.

In response to the podcast, investor Gavin Baker made the best case for allowing some chips to flow to China.

Basically, inference (asking the AI model to do stuff) has overtaken training (building the AI model) for chip usage. Since inference dominates now, the key consideration is how to deliver tokens efficiently and the best way to do that is building a unified system across what Jensen calls a “5-Layer Cake” (energy, chips, infrastructure, models, applications).

AI chips are more fungible for the first step of training the AI model but less so on inference.

Yes, China will keep building its own semiconductor industry. But since Nvidia’s full offering — even on older chips and racks — is better than China’s domestic options, there is still some sweet spot to keep Chinese AI’s industry temporarily hooked on Nvidia and building for the “American Stack”.

It won’t be as easy for China to just plug their AI models trained on Nvidia chips into next-gen Chinese chips when they eventually come online.

“TLDR: as labs shift their focus from training to inference, the costs of portability and the upside of co-design to maximize tokens per watt per dollar both rise. Portability is likely to begin decreasing as a result. […]

The networking primitives for this Huawei system are very different than those for Nvidia’s systems and a model that runs well on Nvidia will not run well on that system and vice versa. This means that if a Chinese ecosystem gets momentum, Chinese models might stop running well on American hardware. And when Chinese models run best on American hardware, America is in a better position as this gives America a degree of leverage and control over Chinese AI that it risks losing to an all-Chinese alternative ecosystem.

This architectural fork makes porting and distillation less effective and strengthens the pro-American national security case for selling China deprecated GPUs imo.”

Another key point is that China’s AI labs are focused on open-source AI models. If these open-source models become the standard in the Global South (similar to Android as compared to iOS), that means the majority of the world’s population could be running on a Huawei-designed system. A number of governments have already banned Huawei telecom infrastructure due to surveillance concerns...and that could play out again.

I don’t know what % of Nvidia’s older chips should go to China. But it’s more than 0%.

Anyway, this is all above my pay grade, so I’ll leave you with this incredible AI-generated video of Jensen summarizing the interview.

***

Some other links for your weekend consumption:

A breakdown of the best Artemis II photos…by Hank Green.

Andy Jassy’s Amazon annual letter…has some very interesting stats. AWS is at a $142B annual run rate. AWS AI revenue is at a $15B run rate after 3 years (this is 260x larger than AWS run rate of $58m after 3 years). Amazon’s chip busines is “on fire”, at a $20B run rate (it would be a $50B business if Amazon sold Graviton, Trainium, Nitro sold chips directly instead of monetizing through the cloud). Then, here are two macro stats that make the Amazon long-term bull case: 1) 80% of retail is still in physical stores; and 2) 85% of IT spend is still on-prem.

Maybe the most actionable LinkedIn post I’ver ever seen…and it explains how to talk to conspiracy theorists.

…and them wild posts:

Finally, here is your weekly “have we reached peak AI bubble yet” piece of news.

Allbirds — the sustainable wool shoe brand that paired perfectly with every Patagonia vest in Silicon Valley over the past decade — is trying to pull off one of the most absurd business pivots in history.

During peak liquidity / stupidity of 2021, Allbirds went public and hit a peak valuation of $4B. It fell 99% before declaring bankruptcy. Then the pivot: on Wednesday, the company said it was rebranding as NewBird AI and is expected to raise $50m to “acquire high-performance, low-latency AI compute hardware and provide access under long-term lease arrangements, meeting customer demand that spot markets and hyperscalers are unable to reliably service”.

We are all dumber for having read that press release.

Bloomberg’s Matt Levine points out that the pivot isn’t from shoes-to-AI. It is shoes-to-meme stock. Whoever is making the $50m investment — which still needs to be approved by shareholders — is getting some juicy upside:

The other level is that Allbirds is pivoting its stock to being an AI meme stock. That definitely worked out! The stock closed yesterday at $2.49 per share, for a market capitalization of about $22 million. Allbirds previously agreed to sell its sneaker business for $39 million and pay out the net proceeds to shareholders as a dividend; the $22 million market capitalization represented, roughly, the expected value of the dividend. At noon today, the stock was at $18.82, up 655% from yesterday’s close, for a market cap of about $164 million. That represents, uh, I guess it represents the expected value of the future AI-native cloud solutions business? Let’s go with that. […]

The proxy does not disclose who the “institutional investor” is but, you know: great trade! The investor is essentially buying $50 million worth of stock at the old, defunct-sneaker-company price, and selling it at the new, AI-neocloud-company price.

Maybe! Presumably the investor can’t sell the stock yet: The convertible financing hasn’t closed, the company needs shareholder approval to allow conversions into stock, and probably selling twice the market cap of the company into the market would take time. (Though more than 200 million shares had traded by noon today, up from about 63,000 yesterday.) The investor has a lot of downside protection, but fundamentally it is betting that the new, AI-neocloud-company price will hold up for a while.

As of this writing, Allbirds is worth $94m. None of this is investment advice.

On the topic of should NVDA sell chips to China and the scenario of an emerging Chinese Tech Stack. One of the positives of deglobalization is how it might counteract the homogenization of culture. It's good that different lands go their own way.